Aggregate supply is the total goods and services that producers are willing and able to supply (produce) at a given price level.

Detailed Explanation:

Understanding aggregate supply is necessary for comprehending the relationship between inflation, employment, and gross domestic product (GDP). The aggregate supply curve is a graph showing the relationship between an economy’s real gross domestic product (RGDP) and its price level.

Short-Run Aggregate Supply Curve

Higher price levels caused by a growing aggregate demand drive companies to increase production to meet the growing demand before the capital structure is measurably changed. Short-run changes are challenging because it takes time for companies to increase their capacity with new plants or equipment. Instead, manufacturers respond to the rising aggregate demand by increasing the utilization of their existing factors of production by requiring employees to work longer hours or adding a shift at the plant.

In the short run, the prices of the factors of production and the final goods and services change at different rates. These discrepancies provide opportunities for businesses. Profits rise when the price of the final good or service increases more (on a percentage basis) than the cost of providing the good or service. When this happens, companies increase production. Profits drop when the input prices rise faster than the price of the good or service. In these cases, suppliers are willing to furnish less. The different timing of price changes in the factors of production market explains the positive slope of the short-run aggregate supply curve.

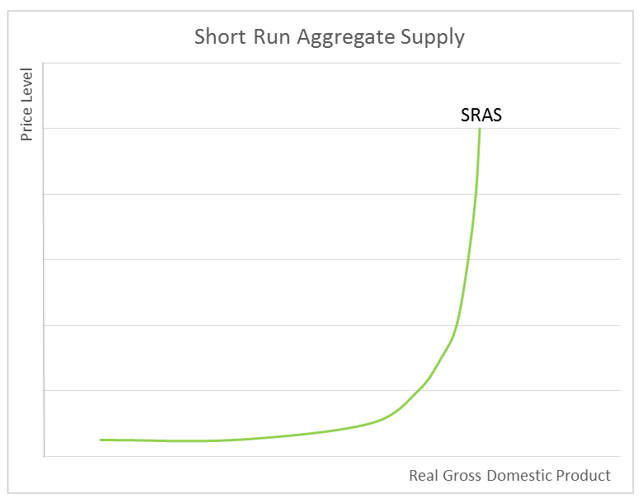

Graph 1 is a short-run aggregate supply curve (SRAS). The economy’s price level is on the vertical axis, and its output measured in RGDP is on the horizontal axis. It slopes upward because producers would take advantage of the short-run price increase and boost production as the price level increases.

Graph 1

Long-Run Aggregate Supply

An economy’s potential production is limited by the resources available, or its factors of production. Economists assume that all prices and costs eventually increase to the same price level at the same rate. In other words, a price level change will not impact production in the long run, resulting in a vertical long-run aggregate supply curve. Instead, permanent changes derived from improved technology or a larger or better educated workforce increase the long-run aggregate supply curve.

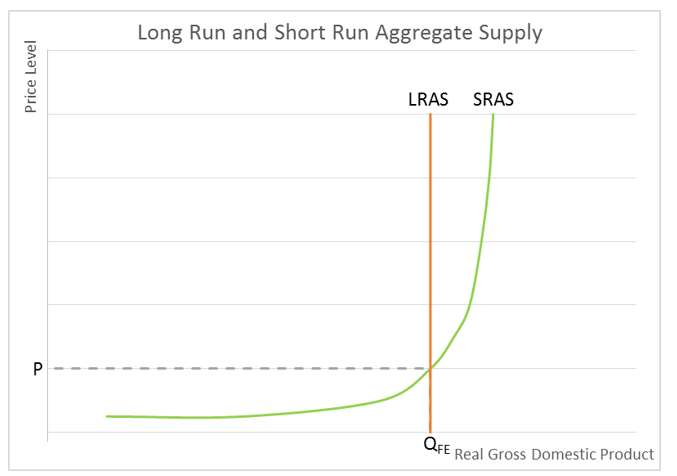

The economy’s long-run aggregate supply curve has been added in Graph 2. P is the price level where the long-run and short-run aggregate supply is in equilibrium.

Graph 2

Here's a video that explains Aggregate Supply in more detail: