A bank run occurs when many depositors simultaneously request to withdraw their deposits.

Imagine that you have most of your savings deposited at a local bank. However, you suddenly learn that the bank has run out of money and cannot fulfill withdrawal requests. You and most other depositors panic and desperately try to withdraw your funds. This situation describes a bank run.

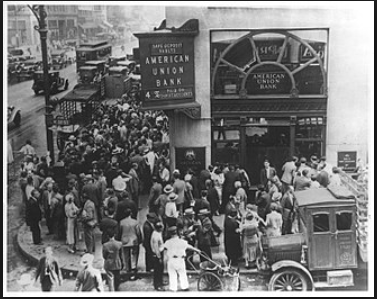

Panic typically causes bank runs and can have severe economic consequences. During the Great Depression, bank runs were widespread and significantly impacted the banking industry. To understand the repercussions, you can listen to an interview of Raymond and Anna Marie McIntyre about how they survived the Depression.

Image from Commons Wikimedia

Bank Run on American Union Bank April 26, 1932

Banks hold a small percentage of their deposits in cash. If reserves are inadequate, a bank may be compelled to sell some of its assets at lower prices. In severe cases, it may result in insolvency. That happened to Silicon Valley Bank (SVB) in March 2023. On March 9, SVB experienced a digital bank run. Depositors attempted to withdraw $42 billion, resulting in the bank’s negative $968 cash balance. SVB, primarily serving startups and venture capital firms, had to be rescued by the Federal government on March 10, making it the second-largest bank failure in US history. Subsequently, Federal regulators seized Signature Bank (SBNY) two days later, and First Republic was closed on May 1. In each case, most of the bank’s customers deposited more than $250,000, the maximum insured by FDIC. With concerns their money was uninsured, many depositors withdrew their money.

Images from iStock

SVB’s deposit base surged from approximately $50 billion to $200 billion between 2019 and 2022, primarily due to its association with startups and venture capital firms. Meanwhile, lending activity slowed down, leading to a surplus of deposits. Management had to do something with its excess deposits. It chose to invest them in government securities. Unfortunately, when interest rates rose, the value of these securities significantly declined. This would not have been an issue if SVB held the securities until maturity.

Meanwhile, a recession and turmoil in the tech industry prompted cutbacks in venture capital funding. As a result, startup companies withdrew their deposits to fund operations, causing outflows to surpass inflows in early 2023. To meet the withdrawals, SVB had to sell a portion of its bond portfolio at a substantial loss. Word spread, triggering the bank run.

Confidence in the banking industry and the overall economy depends on depositors trusting that their funds are secure. Thankfully, safeguards have been implemented in most countries to prevent such occurrences. In the United States, the Federal Deposit Insurance Corporation (FDIC) provides deposit insurance, insuring deposits up to $250,000 per account in member banks. The FDIC was established in 1933 following numerous bank runs during the Great Depression. Its primary objective is to maintain confidence in the US banking system. The Federal Reserve Bank plays a vital role in preventing panics by acting as the lender of last resort. A troubled bank can visit the Federal Reserve’s discount window and borrow the necessary funds when they fear a bank run, which helps stabilize the banking system.

Fractional Reserve Banking and The Creation of Money

Business Cycles

Monetary Policy – The Power of an Interest Rate

Gross Domestic Product – The Power of an Interest Rate

Fiscal Policy – Managing An Economy By Taxing and Spending

{kind=link}