Compound interest is interest earning interest. The interest paid on the principal amount invested continues to compound because it earns interest when reinvested.

Understanding the power of compound interest is easier when comparing it to simple interest. Let’s consider two equal investments: one earns simple interest, while the other earns compound interest. With simple interest, you only earn interest on the principal amount invested. For instance, bonds pay simple interest. If you invest $10,000 in a ten-year bond with a five percent annual interest rate, you will earn $500 ($10,000 * 0.05) each year until the bond matures. The original investment amount of $10,000 remains unchanged, and over ten years, the bond would earn $5,000 in interest.

An investment earning compound interest adds the interest in the preceding years to the initial investment, so the invested amount increases by the interest earned. That is what is meant by “interest earning interest.” For example, a $10,000 ten-year CD that compounds at five percent annually will earn $6,288.95 interest over the ten years. Use the investment calculator to the left to illustrate. $10,000 is the initial investment. The interest rate equals five percent. Only an initial $10,000 investment is made, so the regular investment is left blank. The term is ten years, and the interest compounds annually. After calculating, you should see that the total value equals $16,288.95 or the sum of your initial $10,000 investment and $6,288.95 interest. In the first year, the interest is $500, or five percent of $10,000 (the same as simple interest). However, in the second year, the original $10,000 investment earns $500, and the $500 interest paid in the first year earns $25 interest ($500*.05), bringing the total value to $11,025, or $25 more than if the investment earned simple interest. After ten years, an investor would earn $1,288.95 more when the interest compounds annually.

Banks often compound interest monthly or daily. A shorter compounding period increases the return. For example, switching from annual to monthly compounding increases interest earned to $6,470.09, while daily compounding yields an even higher return of $6,493.42.

The mathematical formula for calculating the final value when interest is compounded annually is:

Future Value = P(1+i)n

Where P is the initial principal invested, i is the interest rate, and n is the number of compounding periods.

Future Value = $10,000 P(1+.05)10

The “rule of 72” is a quick way to calculate when an investment will double if it compounds annually. Divide 72 by the interest rate (not expressed as a decimal) to determine the number of years required to double the investment. For example, assume a $10,000 investment earns ten percent. The rule of 72 would estimate that the investment would grow to $20,000 in 7.2 years. Using the calculator, we see that $20,000 is reached in the seventh year.

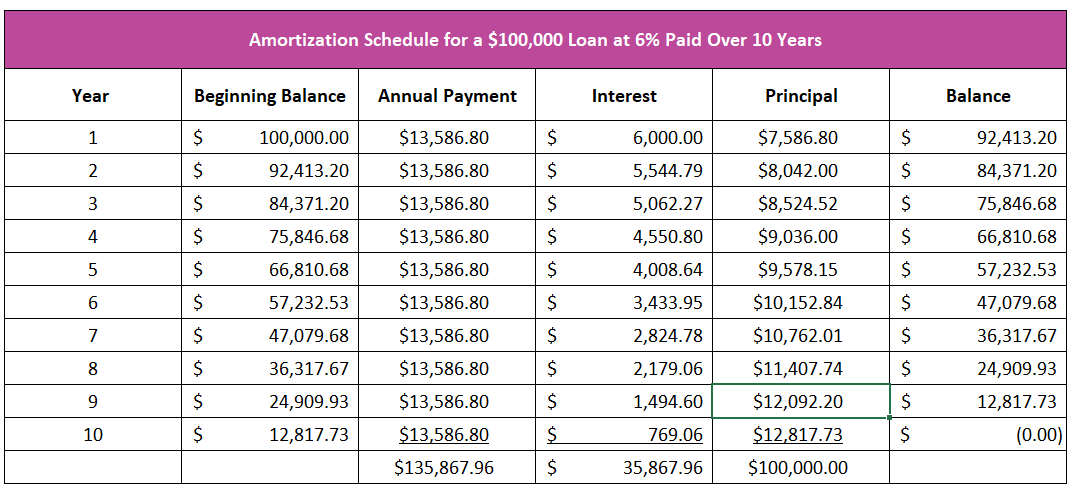

An amortization schedule shows how each payment allocates interest and principal. It helps clarify how debt works by illustrating the benefits of paying a loan off early and the cost of making minimum payments. Interest is the cost of using money. It is paid first before any principal, which means the larger the loan balance, the greater the interest.

For example, suppose Joy has a ten-year loan of $100,000 with an interest rate of six percent. To simplify, assume she makes one annual payment of $13,586.80 and that interest compounds annually. The table provides the amortization schedule for this loan. It’s evident from the schedule that Joy will pay more interest in the early stages of the loan.

Joy pays $6,000 interest (6% of $100,000) in the first year. The principal is the amount remaining after paying the interest. After the first payment, the reduction in principal would equal $7,586.80, which is the difference between the $13,586.80 payment and the $6,000 in interest. That leaves an end-of-year balance at $92,413.20, calculated as $100,000 minus $7,586.80.

In the second year, the allocation to principal and interest would be $9,042 to principal and $5,544.79 to interest after the second payment of $13,586.80. The interest cost is lower in this case because interest is only charged on the remaining balance of $92,413.20.

Table 1

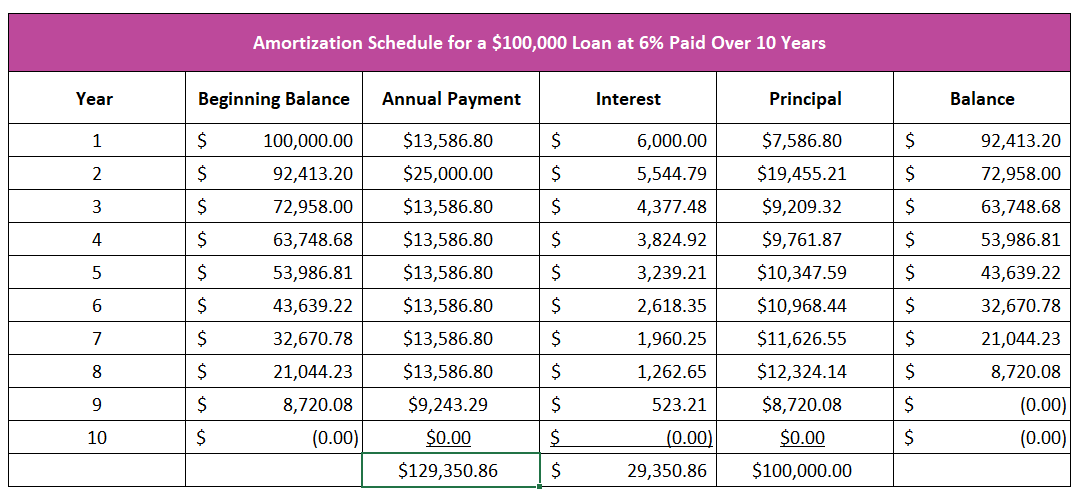

The table below shows how Joy can repay her loan more quickly and save money by making larger payments than the minimum required. If Joy makes a $25,000 payment in the second year and the minimum required payment in the other years, she would pay less interest each year, ultimately paying off the loan sooner. The larger payment saves more than just the additional principal paid, as it reduces the cost of future interest on any remaining loan balance. By making one larger payment, Joy would save $6,517.10.

Table 2

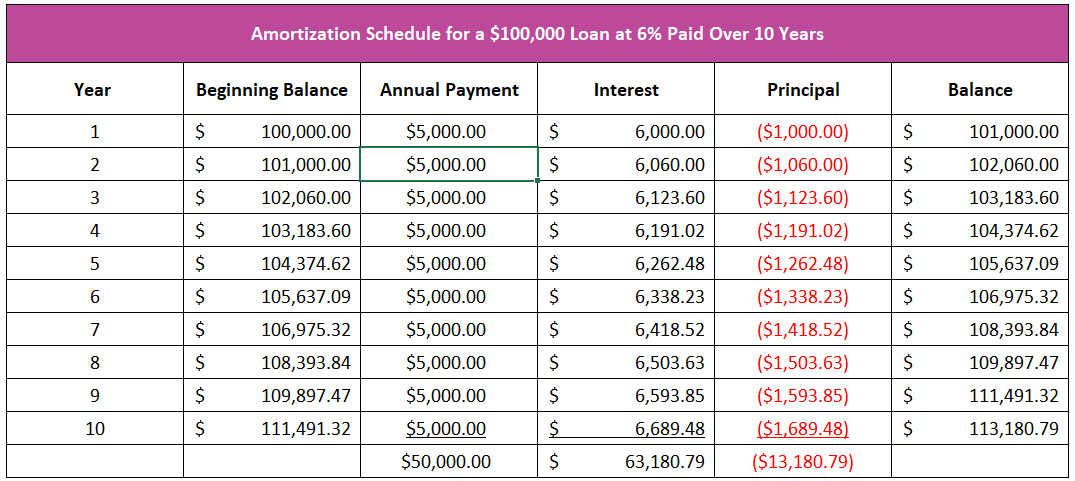

Many people and businesses have learned a hard lesson about compounding after securing a negatively amortizing loan. Negative amortization happens when the payment is insufficient to cover the owed interest. Compounding ends up hurting the borrower. Like any loan, interest is paid first, so the amount of interest not covered by the payment gets added to the loan balance. Table 3 below illustrates how Joy would end up owing more than the original loan if she paid $5,000 each month, which is less than the interest. After ten years, Joy would owe $113,180.79.

Table 3

Opportunity Cost – The Cost of Every Decision

Capital – Financing Business Growth

The Federal Budget and Managing The National Debt