Credit easing is a form of quantitative easing in which a central bank increases the money supply by purchasing specific assets to add liquidity to the banking system and stimulate the economy.

Detailed Explanation:

Central banks influence benchmark interest rates, such as the federal funds rate and LIBOR, by buying and selling government securities. LIBOR, or the London Interbank Offered Rate, is the average rate international banks charge each other for short-term loans. During recessions, central banks increase the money supply and lower lending rates to encourage borrowing. However, when these rates reach zero, traditional monetary tools become ineffective.

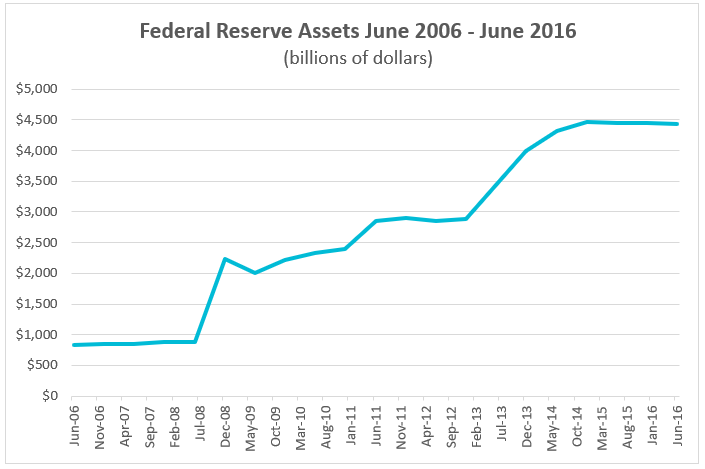

To address this, central banks begin purchasing various financial assets…any financial asset… and creating bank reserves (money) by depositing the amount paid for these assets into the seller’s bank account. This is precisely what the Federal Reserve and other central banks did following the Financial Crisis in 2008. Between December 2007 and early 2015, the Federal Reserve’s assets rose from $0.89 trillion to over $4.5 trillion.

What happens when depositors grow anxious about their bank’s safety and lenders are hesitant to extend credit? Adding liquidity to the banking system enables banks to manage a rise in withdrawals from worried depositors without selling assets at a significant loss. It also helps build confidence among lending institutions, encouraging them to lend money rather than hoard cash. Unfortunately, during the 2008 financial crisis, lenders became more stringent in their underwriting practices. They opted to increase their excess reserves, fearing the crisis would hasten withdrawals and increase their portfolios of nonperforming loans.

Purchasing financial assets also lowers interest rates. The price of bonds and other interest-sensitive assets are not immune to the law of supply and demand. When the demand for a bond increases, its price also increases. As the price goes up, the interest rate falls. For example, if the mortgage rate equals five percent, and the price of the mortgage equals 100, then the yield on the mortgage equals five percent. But if the price increases to 101, the investor’s yield decreases. (Watch our videoto learn how an increase in the price of a bond reduces its interest rate.)

Loans are bought and sold, so when there is uncertainty about the quality of a loan, investors will either choose to avoid purchasing the loan or demand a very low price. Credit easing is a type of quantitative easing that identifies specific interest-sensitive assets to buy. Purchasing the assets adds liquidity and reduces interest rates. During the Great Recession, there were doubts about the credit quality of many assets. Some sub-prime loans had been sold as investment-grade investments when their real value was unknown. Discomfort with the credit ratings resulted in investors discontinuing their investment in mortgage-backed securities or paying a significant discount because of the added risk. This widened the interest rate spread between Treasuries and other debt to historically elevated levels.

For example, the Fed invested over a trillion dollars in mortgage-backed securities (MBS). On June 16th, 2016, the Federal Reserve owned over $1.7 trillion in MBS. In December 2008, the Federal Reserve did not own any MBS. This enormous investment increased demand for MBS, which increased the price, lowering the interest rates of mortgages while providing liquidity to the market. The Federal Reserve’s objective was to lower mortgage rates, thereby attracting home buyers and renewing confidence in the marketplace.

Another targeted asset was commercial paper. There was a growing concern that issuers of commercial paper would not be able to roll over the paper when it matured (i.e., pay it back by issuing more paper). The added investment risk increased the reissue rate. When the Federal Reserve purchased commercial paper, it added liquidity while lowering the rate on commercial paper (since the demand increased). The European Central Bank used the same strategy to purchase corporate bonds.

Credit easing carries some risk, especially given its magnitude between 2008 and 2014. One risk is losing money on the investments. Another factor is inflation, which can be generated by increasing the money supply.