Equilibrium

View FREE Lessons!

Definition of Equilibrium:

Equilibrium occurs when the quantity of a good or service supplied equals the quantity demanded, or when all willing buyers are satisfied and producers do not have any wasted inventory. Equilibrium is also referred to as market equilibrium. On a supply and demand graph, it is where the supply and demand curves intersect.

Detailed Explanation:

Buyers and sellers meet in the market to determine the price and quantity produced of a good or service. They reach an agreement when supply and demand are at equilibrium. Equilibrium occurs when the price at which the quantity suppliers are willing to produce equals the quantity buyers are willing to purchase.

Let's use the market for teenage babysitters in Oak Grove to illustrate equilibrium and how the market responds when out of equilibrium.

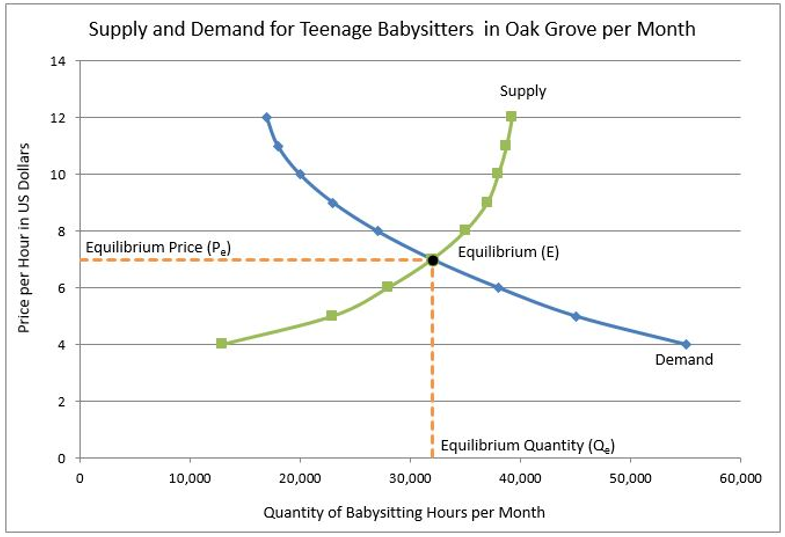

Equilibrium for teenage babysitters in Oak Grove occurs at a price of $7.00 per hour and a quantity of 32,000 hours. At $7.00, sitters are willing to provide 32,000 of babysitting, which is exactly the same number of babysitting hours customers are willing to purchase at $7.00 an hour. On a supply and demand graph, it is the price and quantity where the supply and demand curves intersect.

A shortage results when the quantity supplied is less than the quantity demanded at a given price. Shortages exist at all prices below the equilibrium price. Consumers will bid prices higher to provide suppliers a greater incentive to produce more. For example, at a price of $6 per hour, parents would demand 38,000 babysitting hours, but sitters would only be enticed to provide 28,000 hours. In such a case, there would be a shortage of 10,000 hours. Some parents would struggle to find a babysitter and bid the price up to find someone to sit for their child. Hotels may increase the price of their rooms when a large event is in town because there is a shortage of rooms.

A surplus occurs when the quantity demanded is less than the quantity supplied at a given price. Market forces will push the price down to equilibrium. Returning to our babysitting example, at $8 per hour sitters would be willing to provide 35,000 hours, but parents would only be willing to purchase 27,000 hours, resulting in a surplus of 8,000 hours. Some babysitters would cut their rate to get more business, and others might leave the business. In retail stores, the excess supply becomes evident with mounting inventories. A “clearance” sale will probably follow to bring down the price and generate sales.

Whether there is a shortage or surplus, market forces will move the price and quantity to equilibrium where the quantity sellers supply equals the quantity buyers demand.

Dig Deeper With These Free Lessons:

Supply and Demand – Producers and Consumers Reach Agreement

Changes in Demand – When Consumer Tastes Change

Changes in Supply – When Producer Costs Change

Supply and Demand – The Costs and Benefits of Price Controls