Excess reserves are the reserves exceeding the reserve requirement held in a bank’s vault or on deposit at a Federal Reserve Bank.

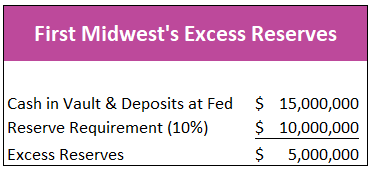

A bank can use its excess reserves to originate loans. Banks are unable to lend all of their deposits because they need some cash to cover their daily withdrawal requests and operating expenses. Assume customers have $100 million on deposit at First Midwest. The reserve requirement is 10 percent. First Midwest must maintain $10 million in reserves ($100 x .10). First Midwest has $15 million in its vaults or on deposit at a regional Federal Reserve Bank, so the bank would have $5 million in excess reserves.

When a bank's excess reserves are negative the bank would need to secure additional cash to meet the reserve requirement. A bank could borrow from other banks at the federal funds rate or go to the Federal Reserve’s discount window and borrow at the higher discount rate. If the excess reserves have not been used to originate loans, they are frequently loaned on a short-term basis to other banks that need to add to their reserves. The Federal Reserve started paying interest on a bank’s reserves in 2008.

Monetary Policy – The Power of an Interest Rate

What is Money

Fractional Reserve Banking and The Creation of Money