A liability is a debt or obligation that needs to be repaid.

A liability is a claim against assets because it must be repaid, and usually, the source of repayment is an individual’s or company’s assets. For example, when a household receives an electric bill, the amount owed is a liability. It is paid using a family’s asset, most likely cash. Businesses incur liabilities in their ongoing activity. A business may secure a bank loan to fund the expansion of a plant or acquire equipment. The borrower has a responsibility to repay the loan. Repayment requires economic sacrifice since cash or some other asset is used to make payments. Three types of liabilities are: current liabilities, long-term liabilities, and contingent liabilities.

Current liabilities are due in less than one year. The electrical bill mentioned above is a current liability. Other current liabilities include accounts payable to vendors, wages payable to employees, or taxes payable to the government. A loan or a portion of a loan that is due in one year is also a current liability.

Long-term liabilities are debt obligations that exceed one year. They include mortgages, long-term bank loans, and bonds that are issued by a corporation or government. (A bond is an asset for the entity that purchases it, but a liability for the party that sells the bond.)

Contingent liabilities include potential obligations that may impact a company’s financial health. For example, if it is probable a company will lose a lawsuit, the estimated settlement would be listed as a contingent liability. Assume a former employee is suing Bill's Grill for negligence after suffering burns. His estimated settlement is $500,000. Bill's Grill would have a contingent liability of $500,000.

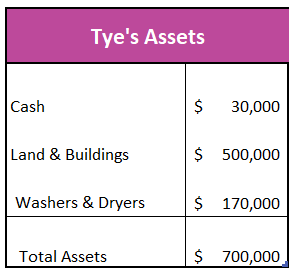

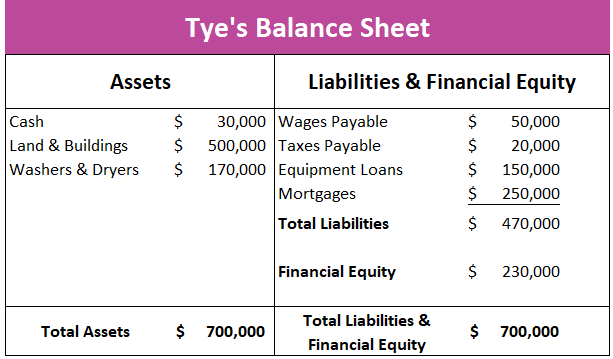

Liabilities are listed on the right side of a balance sheet. A balance sheet can be broken into three components: assets, liabilities, and financial equity. The sum of a company’s liabilities and financial equity must equal its assets since the value of a company (equity) equals the sum of its assets minus what it owes (its liabilities). For example, assume Tye’s Laundry has $700,000 in assets and $470,000 in debts. Tye has $230,000 in financial equity in the company. This is reflected on Tye's balance sheet where all of his assets are listed on the left side, and the liabilities and financial equity are listed on the right side. Tye’s Laundry has the following assets:

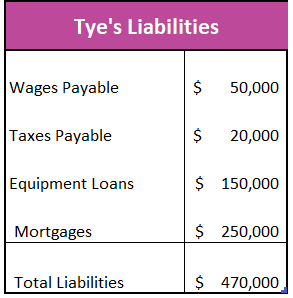

Tye’s Laundry has the following liabilities:

Tye’s ownership interest, or financial equity, equals $230,000 (assuming Tye is the only owner).

When expressed on a balance sheet, the financial statement would be:

Capital – Financing Business Growth

Fractional Reserve Banking and The Creation of Money

Fiscal Policy – Managing The Economy by Taxing and Spending

The Federal Budget and Managing The National Debt