Perfect competition is a market structure where many sellers and buyers trade in identical products. Neither seller nor buyer is powerful enough to influence the market price.

Perfectly competitive industries are rare because there are few industries with many sellers and buyers where the producers sell identical products, and where no single buyer or producer has any market power. Most economists use the grain market as an example of a perfectly competitive industry. Perfect competition has the following characteristics.

Companies in a perfectly competitive industry sell standardized, or identical, products. For example, a buyer of wheat cannot tell if Farmer Jones or Farmer Sue produced the bushels they buy. Standardization prevents companies from increasing their price by differentiating themselves from their competition.

Companies in other market structures differentiate their products to build brand loyalty which enables them to raise their prices. Products and services may be differentiated by offering better service, slightly distinctive characteristics, or even different packaging. This market strategy is unavailable to companies in perfectly competitive industries because they sell standardized products.

For example, assume Farmer Jones’s farm is 5,000 acres. In the year 2000, approximately 520 million acres were used to grow wheat, so while a 5,000-acre farm is large, it is not large enough for Farmer Jones to have an impact on the market price of wheat, since he produces only 0.01 percent of the market. Wheat has many buyers because of its widespread uses. Large food companies like General Mills and Kellogg’s buy enormous amounts of wheat, but even these large firms do not have sufficient clout to impact its price. The price of wheat is instead determined on the Chicago Board of Trade, in the same way the price of a stock is determined on the New York Stock Exchange. Perfectly competitive markets must have enough buyers and sellers that no buyer or seller is able to alone influence the price of the good or service. The price is determined in the marketplace by supply and demand.

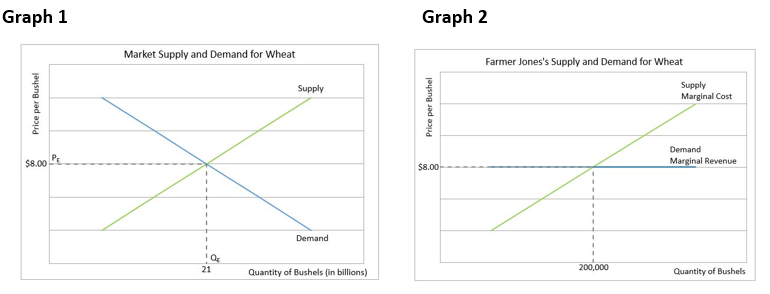

Assume the price of wheat is $8.00 a bushel. If Farmer Jones tried to increase his price to $8.25, he would not be able to sell any of his wheat. His sales would drop to zero! Frequently a business will lower its price to sell more of its goods or services, but this strategy does not make sense for Farmer Jones. There is no incentive for him to sell at $7.75 because he can sell his entire harvest for $8.00 a bushel. Farmer Jones is a price taker. He accepts the price the market dictates. The only way Farmer Jones can increase his revenue is by increasing production. Farmer Jones’s situation is illustrated by Graphs 1 and 2. Graph 1 shows the market equilibrium and market price using the industry supply and demand curves. The market price, PE, is $8.00 per bushel. The entire industry produces 21 billion bushels (QE on Graph 1).

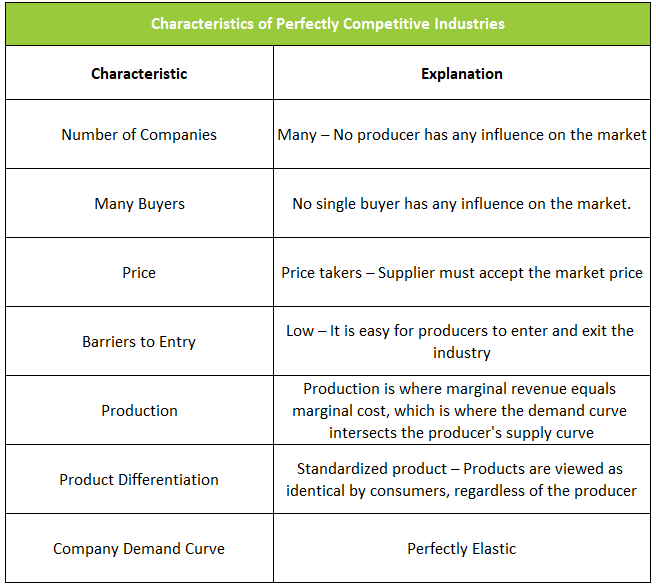

Graph 2 provides Farmer Jones’s supply and demand curves. He produces 200,000 bushels, which is a tiny fraction of the total market. Farmer Jones has virtually no effect on the market supply. He has no bargaining power, so he must accept the market price. His demand curve is horizontal (perfectly elastic) because if he raised his price he would be unable to sell a single bushel, but he does not have an incentive to lower his price since he can sell all he produces without influencing the market price.

The demand curve is also Farmer Jones’s marginal revenue curve. Marginal revenue is the additional revenue from selling one additional unit of a good or service. Farmer Jones does not have to drop his price to sell even one additional bushel of wheat, so his demand curve is also his marginal revenue curve. Farmer Jones’s supply curve is determined by his costs, the weather, and the productivity of his land. The supply curve represents Farmer Jones’s marginal cost to produce a bushel of wheat. Farmer Jones’s most profitable production level is where the revenue derived from selling an additional bushel equals the cost to produce that final bushel, or where his marginal revenue equals his marginal cost.

Next year Farmer Jones would probably choose to substitute rye for wheat if his expected profit for rye is higher than wheat. Fortunately, he can easily choose to switch to rye because of a low barrier to entry. (Note that the capital – productive land and equipment - required to start a farm may be a high barrier to entry, but Farmer Jones has a low barrier to switch to rye because he already owns the land and equipment.)

Entrepreneurs may choose to start a business if they see another company earning a large profit. Lower barriers to entry make it easier for entrepreneurs to enter the market, thereby increasing competition. The Internet has reduced the barriers to entry in many industries. For example, eBay and Amazon have broken geographical barriers by opening markets for entrepreneurs in areas far from home.

The table below summarizes the common characteristics of a perfectly competitive industry.

Market Structures Part I – Perfect Competition and Monopoly

Market Structures Part II – Monopolistic Competition and Oligopoly

Output and Profit Maximization

Supply and Demand – Producers and Consumers Reach Agreement