A product has a perfectly inelastic supply when the quantity supplied is the same regardless of price. The product's supply curve is vertical.

The Mona Lisa painting by Leonardo da Vinci has a perfectly inelastic supply curve. There is only one Mona Lisa painting, and it cannot be duplicated at any price.

Because the Mona Lisa is unique, it will always have a perfectly inelastic supply. In most cases, time has a great influence on the elasticity of supply. Production of some goods or services cannot be increased in the very short term. Time provides greater elasticity in the production of almost all goods and services. Over time management can invest in the labor and equipment to increase production, or lay off workers and find other uses for their plant and equipment If prices fall.

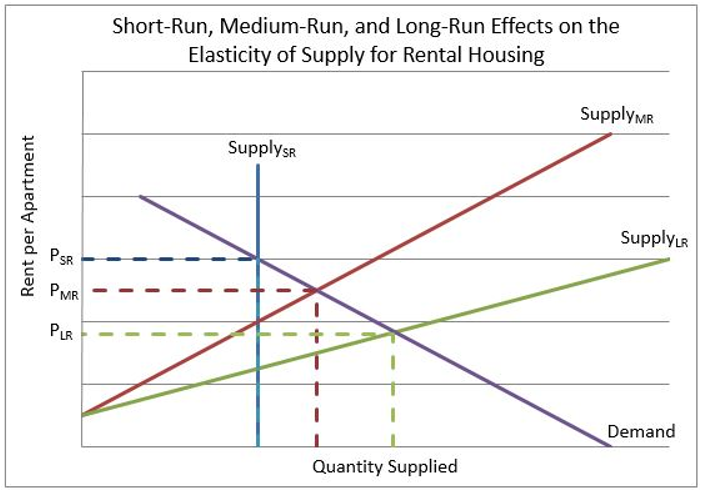

The supply of rental housing is a good example. Assume town commissioners pass regulations that generate a huge increase in the demand for rental housing. Increasing the supply of rental housing overnight is virtually impossible, so the immediate supply curve is perfectly inelastic. Because a perfectly inelastic supply is unaffected by price its supply curve is vertical It is shown as SupplySR on the graph below. The immediate impact of the regulation change is a large increase in price (rent), represented by PSR. Some homeowners, prompted by the sudden increase in market rents, will quickly convert basements or spare bedrooms into small apartments. The medium-run supply curve is SupplyMR. The supply of housing is increased, and the market rent drops to PMR. In the long run, the supply curve will continue to rotate clockwise to become even more elastic. Homeowners and builders will invest more resources in renovating homes and building apartments to meet the community’s needs, making the long-term supply quite elastic. SLR and PLR are the long-run supply curve and price.

Price Elasticity of Supply – How Does a Producer Respond To a Price Change

Supply – The Producer's Perspective

Factors of Production – The Required Inputs of Every Business

Price Elasticity of Demand – How Consumers Respond to Price Changes