A shortage occurs when the quantity of a good or service demanded exceeds the quantity supplied. Shortages occur at prices less than the equilibrium price.

A shortage results when the quantity supplied is less than the quantity demanded at a given price. When tickets sell out in a matter of minutes, there is a shortage. A long waiting list to fulfill an order is also evidence of a shortage. Market forces will push up the equilibrium price. Scalpers may purchase tickets and resell them at a higher price if there is a shortage of seats to an event. In 2021, people had to wait for months for a Tesla to be delivered. Tesla raised its prices.

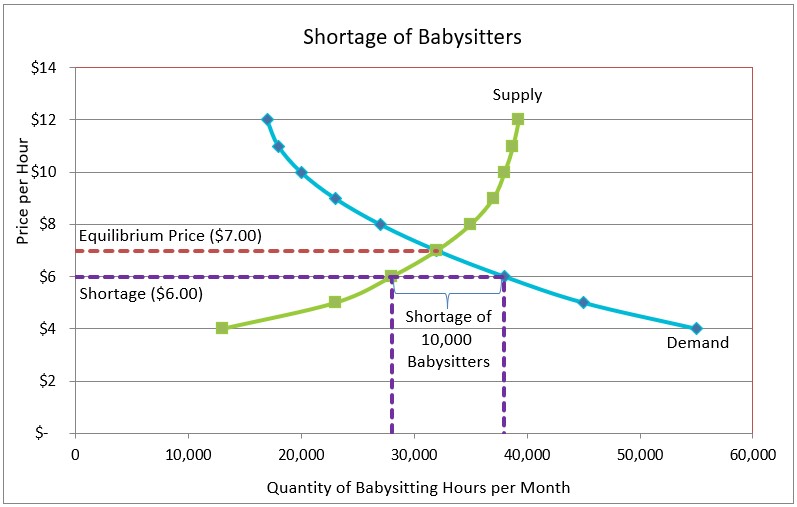

The supply and demand graph below is for babysitters in a community. Shortages exist at all prices below the equilibrium price because the quantity demanded exceeds the quantity supplied. At the equilibrium price, babysitters would provide just enough service to satisfy all the parents—the number of hours demanded equals the number of hours provided. The equilibrium rate (price) is $7.00 per hour, and at that hourly rate 32,000 hours would be purchased. A shortage of hours exists for all prices below $7.00. For example, parents would want to purchase 38,000 hours at $6.00, but sitters would be willing to provide only 28,000 hours at $6 per hour, resulting in a shortage of 10,000 hours. Some parents would bid up the rate to entice a babysitter to serve them. Eventually, the rate would increase to $7.00, the equilibrium.

Supply and Demand – Producers and Consumers Reach Agreement

Supply and Demand – The Costs and Benefits of Price Controls

Changes in Demand – When Consumer Tastes Change

Changes in Supply – When Producer Costs Change