The statutory tax rates are the tax rates that are established by the law. The highest income tax rate a person or business qualifies for is referred to as their “tax bracket”.

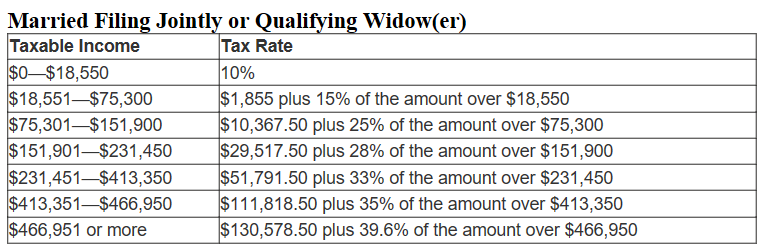

The statutory personal income tax rates are provided in tax tables. Different tax tables reflect the taxpayer’s filing status. For personal taxes, this includes single, married filing jointly, filing as a qualifying widower, or married filing separately. There are also tables for businesses. The statutory tax is calculated by using the appropriate tax table. A taxpayer’s “tax bracket” is determined by his taxable income. For example, a married couple filing jointly with a taxable income of $152,000 is in the 28 percent tax bracket. This means that additional income would be taxed at 28 percent until the taxable income reaches $231,451, at which time the tax bracket would jump to 33 percent. See the tax table below.

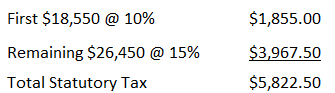

Assume you are married and recently graduated from college. You and your spouse both work and have a combined annual income of $55,000 before tax. You have $10,000 in deductions, resulting in a taxable income of $45,000. Taxable income is gross income less deductions. (In the United States, it is found on Line 43 of Tax Form 1040.) The statutory rate is 10 percent for the first $18,550 you earn. You owe $1,855 on this portion of your income. For the remaining $26,450 the statutory rate equals 15 percent, so you would owe $3,967.50 on the taxable income exceeding $18,550. Your total statutory income tax equals $5,822.50.

It is important to distinguish between the statutory rate and the effective rate. Most governments have deductions and tax credits which reduce the tax further. They are enacted to either provide assistance to a group of people or an incentive for a particular behavior. For example, in the United States the Credit for Child and Dependent Care Services (Line 49 of Form 1040) is a tax credit to provide an incentive for parents to work and lower their after-tax expense for day-care. A tax credit is subtracted from the statutory tax derived from the tax tables. The effective rate is an average rate – and is calculated by taking the tax paid and dividing it by the total income. Continuing with our example, assume you have one child. Last year you paid for child care and the government provides you with a $1,000 credit to help you. Your tax liability is reduced by the full amount of the credit to $4,822.50. Your effective tax rate equals your tax liability divided by your total income (Line 22 on Form 1040), or 8.77 percent. (Note that for corporations, the formula would be their tax liability divided by the profit before tax.)

($4,822.50 / $55,000) *100 = 8.77%

Economists also consider the marginal tax rate. The marginal rate is the tax rate charged on the next dollar earned. For individuals it is normally the tax payer’s tax bracket. If you received a $100 bonus it would be taxed at 15 percent, so your marginal tax rate equals 15 percent. This is the most appropriate rate when determining investment decisions such as whether to invest in a tax free municipal bond.