The supply of a good or service is the number of units producers are willing to sell at a given price over a defined time period.

The supply for a product represents the seller’s perspective. It is the number of goods or services producers are willing to provide at different prices. Generally, businesses are willing to provide more of a good or service at higher prices. The law of supply states that—other things being equal—as a good or service’s price increases, there is an increase in the quantity supplied for that good.

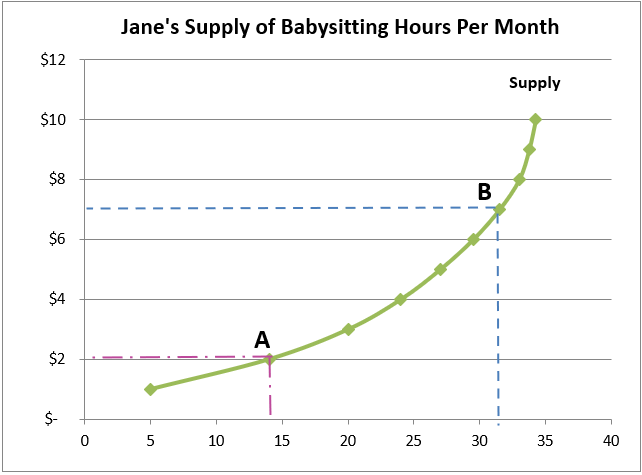

Suppose Jane babysits occasionally to earn some spending money. At low hourly rates, Jane is willing to babysit, but not that often—more as a neighborly gesture than as an income-generating venture. That’s because she would rather look for another job that would pay more or even forgo working and spend more time with her friends. However, at higher rates, Jane would be willing to babysit more because she realizes that she would prefer babysitting to another job that would be more restrictive. The relationship between the price of a good or service and the amount producers are willing to supply is shown on the good or service’s supply curve.

A change in the price of a good or service results in a change in the quantity supplied for the good or service and is illustrated by movement along the supply curve. For example, at $2 per hour, Jane would only be willing to babysit 14 hours per month. However, at an hourly rate of $7, Jane would be willing to babysit 32 hours per month, an 18 hour increase in the quantity supplied. This is shown as moving from point A to point B in the graph below.

As the price increases, more babysitters will enter the market. The sum of every babysitter’s supply curve is the community supply curve. Many variables influence the supply for a good or service – but the most important is the cost to produce it and bring it to market. When the price is too high, suppliers may be willing to offer more of a good or service, but buyers may be unwilling to pay the high price. The merging of the supply and demand for a good or service determines its market price and the quantity produced.

Watch this skit illustrating Jane's thought process in accepting more jobs.