A supply curve is a graph showing the quantity of a good or service that producers offer at different prices during a specific period of time.

A company’s supply curve illustrates the number of goods and services the company is willing to supply at every price. The quantity supplied and price are directly related, meaning that as the price of a good or service increases, the quantity producers are willing to supply increases, and vice versa. The amount a producer is willing to supply of a good or service at a specific price is represented by a point on the supply curve. The production process and outside influences are held constant. Outside influences include the technology, input costs, regulations, the number of firms in the industry, future expectations, regulations, and tax rates. A change in any of these results in a new supply curve, which economists refer to as a change in supply.

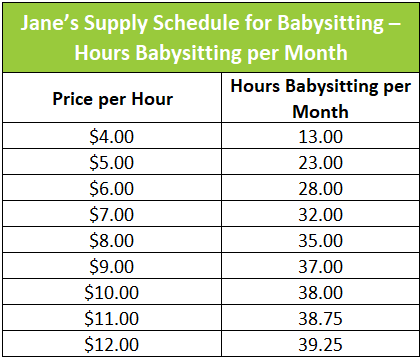

For example, assume Jane is a babysitter. She is willing to work more hours if she is paid a higher wage. The table below is Jane's supply schedule and will be used to graph her supply curve. A supply schedule is a table showing how much of a good or service a supplier is willing to produce at different prices. At the lower prices, Jane may be willing to babysit infrequently, more as a neighborly gesture than as an income-generating venture. At these low prices, she would prefer seeking alternative employment or spending time with her friends. However, as the price increases, Jane realizes that she would prefer babysitting to another job that is more restrictive. Higher prices provide an incentive to forgo hanging out with friends to earn more money.

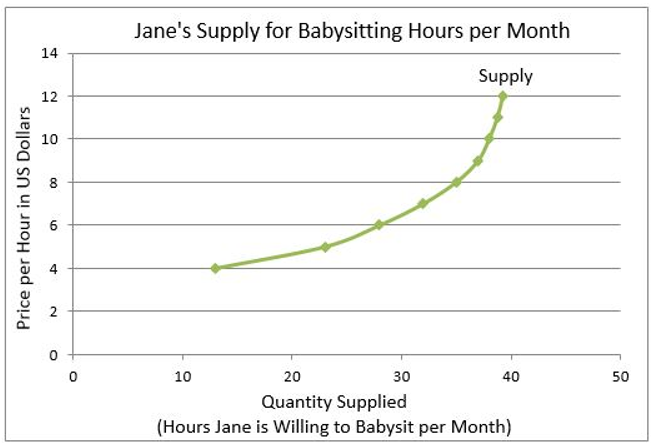

Jane’s supply curve is plotted by plotting the number of hours she would babysit at every price, over a defined period of time. Her wage (price) is on the vertical axis, and the number of hours she is willing to work per month is on the horizontal axis.

The market supply curve is for an entire community and includes all of the babysitters. The market supply curve is drawn by plotting the total number of hours all the babysitters would babysit at each price. Note that the supply curve assumes that the producers' costs and other variables that impact the supply remain unchanged.

Economists plot the demand curve and the supply curve together to determine the equilibrium price and equilibrium quantity of a good or service. At equilibrium, there would not be a surplus or shortage of the good or service.

Supply – The Producer’s Perspective

Changes in Supply – When Producer Costs Change

Price Elasticity of Supply – How Does a Producer Respond to a Price Change

Supply and Demand – Producers and Consumers Reach Agreement

Demand – The Consumer’s Perspective

Factors of Production – The Required Inputs of Every Business