Tax incidence measures the distribution of the tax burden between different groups.

The tax burden or tax incidence is rarely shared evenly. In the case of an excise tax, the party who bears the greatest burden is the party with the more inelastic demand or supply curve, or in other words, the party with fewer options. Consumers bear most of the excise tax when the demand curve is more inelastic than the supply curve. Suppliers bear most of the tax incidence when their supply curve is more inelastic than the demand curve. Intuitively, this makes sense. Consumers with an elastic demand for the good or service (such as ferry crossings) typically have substitutes (such as a bridge). Or they may view the good or service as inessential and decide not to pay the tax. These consumers may choose to use a substitute good or service or to do without it entirely. Conversely, consumers with an inelastic demand are less sensitive to price increases and would be more willing to absorb a tax. They will pay a higher price because they need access to the good or service. Suppliers with an inelastic supply have less flexibility in managing their supply, so they are better off absorbing more of the tax rather than altering production.

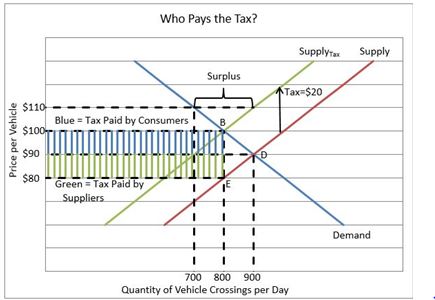

Maritime runs a ferry service. The government has imposed a $20 excise tax. Prior to the tax, 900 vehicles crossed the channel every day and paid $90 per crossing. Following the tax, the equilibrium price increases to $100 and the quantity demanded falls to 800 vehicles. The graph illustrates how consumers and the supplier (Maritime) share the tax burden on ferry crossings. Government tax revenues equal $20 per vehicle. With 800 vehicles crossing each day, the total daily excise tax revenue is $16,000 ($20 x 800). The total tax revenue is shaded green and blue on the graph. One hundred fewer vehicles would ride the ferry each day after the tax is imposed. Those who choose to take the ferry would pay $10 more than before the tax. Since each fare costs $10 more and 800 fares are sold daily, the tax paid by consumers equals $8,000 ($10 x 800). This area is shaded blue on the graph.

Maritime Ferry had hoped to pass the entire tax through to its customers and maintain traffic at 900 vehicles per day, but management quickly realized Maritime was losing business when its traffic dropped. As a result, the company lowered the price to $100. Even after absorbing $10 of the $20 excise tax, the number of daily vehicle crossings dropped from 900 to 800. The excise tax cost Maritime Ferry $8,000 dollars (800 vehicles x $10 per fare) per day. This area is shaded green.

Ultimately the excise tax results in a deadweight loss shown as Triangle BDE on the graph. This area represents the loss of benefits to Maritime Ferry and its customers (i.e., society) resulting from the reduction in ferry rides. A deadweight loss is the loss of economic efficiency that occurs when the marginal benefit does not equal the marginal cost. In other words, it is the added burden placed on consumers and suppliers when the market equilibrium is altered because of the excise tax. A deadweight loss is determined by assessing the loss of production and the higher price when the tax alters the market equilibrium.

Two costs resulting from the excise tax are included in the deadweight loss. First, the equilibrium price increases because the tax pushes the equilibrium price from $90 to $100. Even though the cost per ferry ticket is $10 higher, Maritime is actually losing $10 in revenue per ticket because it must pay $20 per ticket to the government. Second, there is a cost to society of fewer crossings. That is the cost in time and money by making the trip less convenient for some commuters. The equilibrium quantity decreases from 900 to 800 crossings per day.

Who Really Pays an Excise Tax

Managing Supply Using Tariffs, Subsidies, Quotas, and Licenses