The Bureau of Economic Analysis published key December statistics in its publication, Personal Income and Outlays. Here are the key highlights of its report.

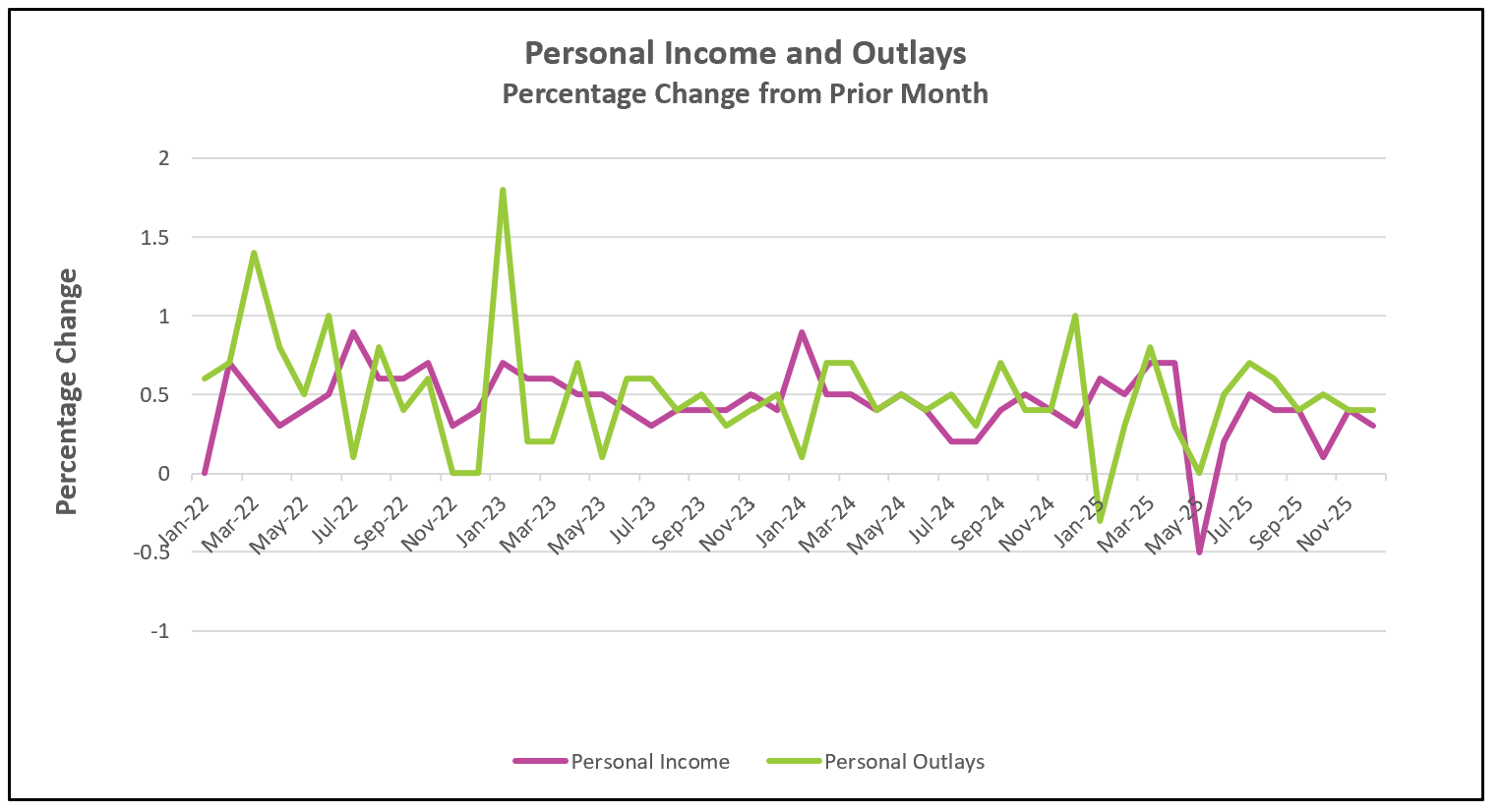

Disposable personal income in December rose only marginally after inflation, leaving many budget-conscious households with little real growth in earnings. While incomes increased by $86.2 billion, much of that gain reflected transfer payments—about $38.4 billion—primarily driven by settlement claims tied to 2023 Maui fire losses paid by utilities and by increased Medicare payments. As a result, real purchasing power barely kept pace with price rises for many families.

Despite the weak real-income gain, consumer spending continued to grow faster than income, implying that part of the spending was funded by higher borrowing and drawing down savings. The personal saving rate fell to 3.6%, the lowest since October 2022, underscoring that households are relying more on debt and accumulated reserves to sustain consumption.

On the earnings side, private-sector compensation gains were concentrated in service industries, while compensation in the goods sector edged down slightly. That divergence reflects ongoing strength in services demand even as goods-producing firms face different pressures.

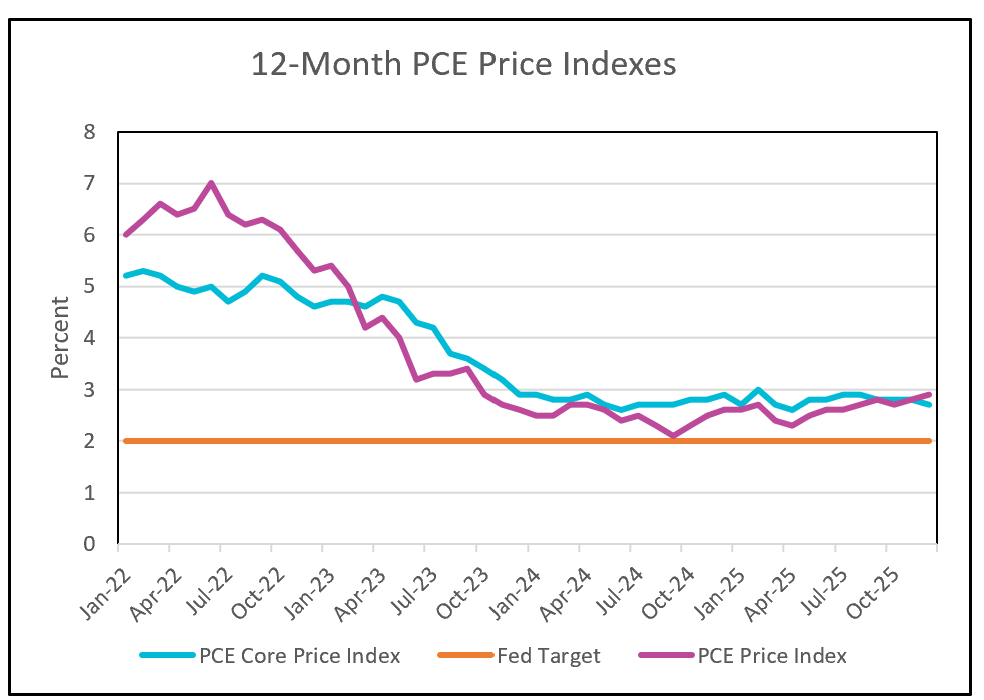

Inflation measured by the PCE price index accelerated: the headline PCE rose 0.4% in December (after 0.2% in November), the largest monthly increase since February 2025, and the core PCE (excluding food and energy) also jumped to 0.4% monthly. Over the past 12 months, the headline PCE was up 2.9% and core PCE was up 3.0%—both the highest year-over-year readings since early 2024. The PCE has been running above the more widely published consumer price index (CPI), partly because the CPI places a heavier weight on housing and car prices; rental and auto price increases have been decelerating, producing a contrast between the rising PCE and the modest drop in the CPI (December CPI 2.7%, January CPI 2.4%).

With PCE inflation remaining above the Federal Reserve’s 2.0% target, policymakers opted not to cut interest rates at their most recent meeting, preferring to see inflation decline further before resuming rate reductions. A few participants even argued that raising the policy rate would be appropriate given the inflationary readings.

The US economy grew by 1.4% according to the recent Advance Estimate from the BEA. (Read Higher Rock’s summary and analysis.) Additionally, the BLS will release its February Employment Summary on March 6th. Higher Rock will provide a timely summary and analysis of each report shortly after its release. Be sure to look out for our forecasts for RGDP, employment, and inflation for 2026, as well as a review of how our 2025 predictions performed, later this month.