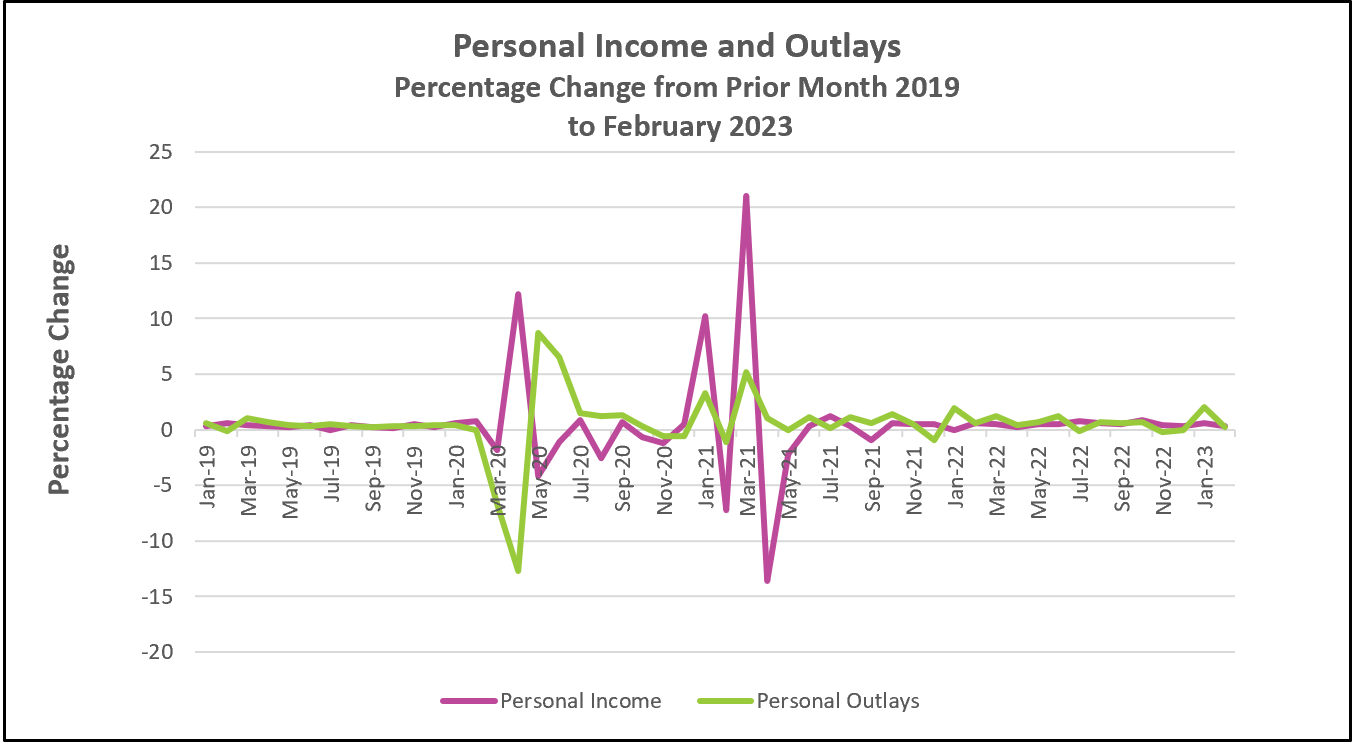

A downward trend in inflation has been reestablished! February’s BEA report reverses January’s readings of many variables influencing inflation. Growth in personal income and outlays both slowed. This data and the recent turmoil among regional banks will decrease the likelihood that policymakers at the Federal Reserve will continue to increase their benchmark rate much longer. Wall Street welcomed the news. The Dow Jones Industrial Average and the S&P 500 rallied 0.6% shortly after the report was released.

The highlights of the Bureau of Economic Analyses’ full report, Personal Income and Outlays – February 2023, are listed below.

The 12-month PCE price index decelerated to 5%, its slowest pace since September 2021. Lower energy costs, which fell 0.4% in February, and less food inflation, which only gained 0.2%, lowered the price index. However, food prices remain high – 9.7% higher than a year ago. The 12-month core PCE price also decreased, reaching 4.6%, its lowest level since October 2021. Economists prefer the core index when evaluating trends because it excludes volatile food and energy prices. Friday’s release reinforced the more highly publicized CPI index, which increased 0.4% in February after rising 0.5% in January. The PCE price index is probably the more important measure of inflation because it is preferred by the Federal Reserve when determining its monetary policy.

Inflation had been trending lower before January. However, January’s spending and income increased the aggregate demand and pushed prices sharply higher. February reestablished the downward trend in prices, personal income, and consumer spending. Growth in personal income supports higher prices by providing consumers with additional money to spend. Low unemployment and a surplus of open jobs to available workers have kept wages barely ahead of inflation. However, before January’s jump, personal income had trended lower. An 8.7% cost-of-living adjustment increase in Social Security payments contributed significantly to the gain.

Spending increased modestly in February. In fact, it fell 0.1% after adjusting for inflation. Americans dined out less. They also spent less on motor vehicles, proving that higher interest rates have deterred sales. An increase in spending on housing, health care, and groceries offset those decreases.

It is good news that inflation has fallen since June 2022, when the PCE price index peaked at 7.0%. While the re-establishment of downward trends in prices, consumer spending, and personal income are encouraging, inflation remains well above the Federal Reserve’s 2% target. Policymakers at the Fed have aggressively combatted inflation by increasing their benchmark rate nine times since last March. Their objective is to reduce aggregate demand by pushing up rates. They have succeeded in slowing sales of large interest-sensitive items such as homes and cars, but consumer spending on everyday items remains high. Higher wages have financed much of the added consumer spending.

March’s collapses of Silicon Valley Bank and Signature Bank brought anxiety to the financial markets. How will banks respond? Would increasing rates (which contributed to the demise of the banks) put other banks in jeopardy? Will some banks lend less to preserve their capital reserve? If so, the banking crisis would slow economic growth in much the same way as a rate increase and may cause policymakers to pause its tightening.

Nevertheless, policymakers have been clear that the failures will not deter them from their main objective – lowering inflation to 2%. This release does not reflect the banking fallout, so FOMC members will be very interested in the economic data released before their next meeting on May 3. The Bureau of Labor Statistics will release its Employment Situation – March 2023 on April 7. Recently, higher wages resulting from a shortage of workers have added inflationary pressures because labor is the highest cost for many service companies. The report will show whether the labor shortage has lessened and whether the upward pressure on wages has subsided. Check back to HigherRockEducation.org for our summary and analysis of this important data.