The U.S. economy entered 2026 on shaky footing, with slowing growth, cautious consumer spending, rising debt, and persistent inflation, likely keeping the Federal Reserve on hold amid growing uncertainty.

The Bureau of Economic Analysis (BEA) published key January statistics in its publication, Personal Income and Outlays. Here are the key highlights of its report.

The latest economic report offers a snapshot of conditions just before the outbreak of war with Iran, making it difficult to draw firm conclusions about the outlook. Even before the conflict, the U.S. economy appeared to be losing momentum. The BEA revised fourth-quarter 2025 growth sharply lower, from an annualized 1.4% to just 0.7%, underscoring a more fragile expansion. At the same time, the labor market showed signs of softening, with payrolls declining in three of the past five months and the unemployment rate edging higher. Inflation remained persistent, as the all-inclusive PCE price index eased only slightly while the core measure continued to climb.

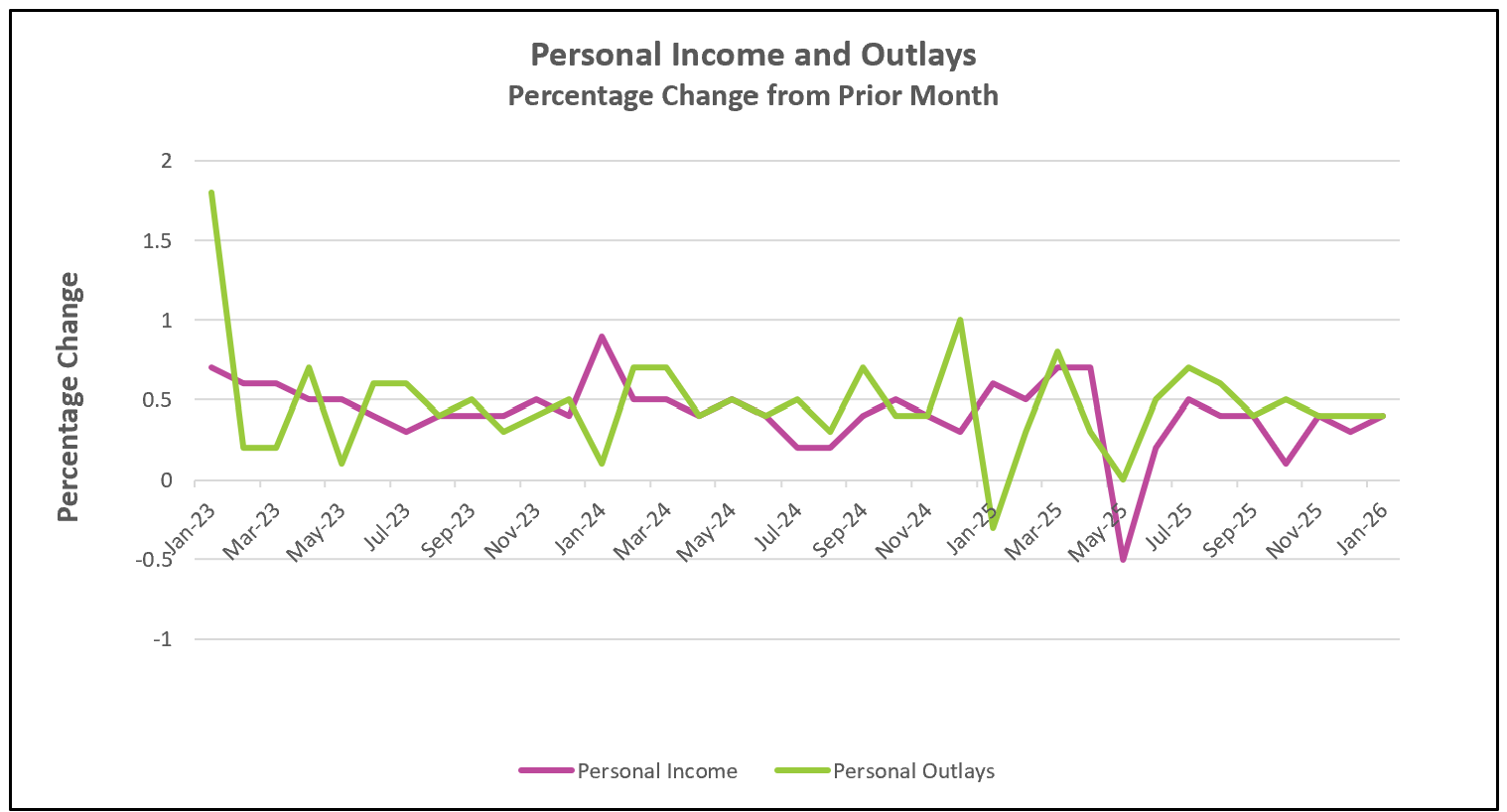

Despite this backdrop, disposable personal income surged in January, supported by a 2.8% cost-of-living adjustment for Social Security recipients, lower tax withholding, and rising wages. However, this income strength did not translate into robust consumer spending. Real spending increased by just 0.1% for the month, suggesting that households are becoming more cautious.

Spending patterns suggest that households are becoming increasingly wary of the economy. Consumers are prioritizing essentials such as healthcare and housing, where spending rose notably, while cutting back on discretionary categories like recreation and apparel. Healthcare, in particular, saw the largest increase. This reallocation suggests growing concern about economic conditions, as consumers typically scale back nonessential purchases when confidence deteriorates. Indeed, the University of Michigan Consumer Sentiment Index dropped to its lowest level of the year.

Both income and spending rose 0.4% in January. Spending has outpaced income for much of the past year, leading to reduced savings and increased borrowing. Many households saved some of their added income. Although the savings rate rebounded to a six-month high in January, debt as a share of disposable income climbed to its highest level in six years. Looking ahead, tax relief and wage gains could support consumption, but elevated gasoline prices may offset these benefits if they persist.

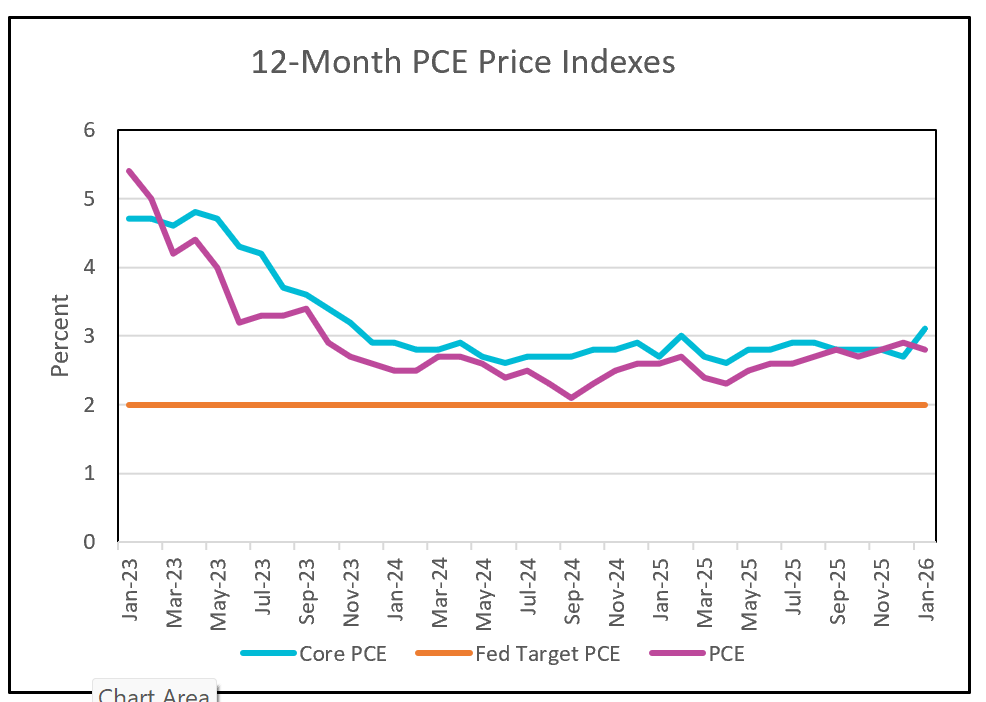

Inflation dynamics remain a central concern for policymakers. The core PCE price index rose 3.1% over the past year, remaining well above the Federal Reserve’s 2% target and continuing an upward trend since mid-2025. Notably, the PCE measure has recently outpaced the more widely followed CPI, partly because slowing rent increases have a smaller impact on PCE. Additionally, rising goods prices since November suggest that tariffs may be contributing to upward price pressures.

Given these conditions, the Federal Reserve is widely expected to hold interest rates steady at its upcoming meeting. While the CPI has shown recent moderation, policymakers place greater weight on the PCE price index, which suggests inflation remains too high. Complicating the outlook further, the war is already weighing on financial markets, raising concerns that wealthier households could begin to pull back spending if market declines persist. Overall, the economy entered this period of geopolitical uncertainty in a more tentative state, with slowing growth, cautious consumers, and stubborn inflation shaping the near-term outlook.