The key findings from the Bureau of Economic Analysis’s Personal Income and Outlays - March 2024 are outlined below.

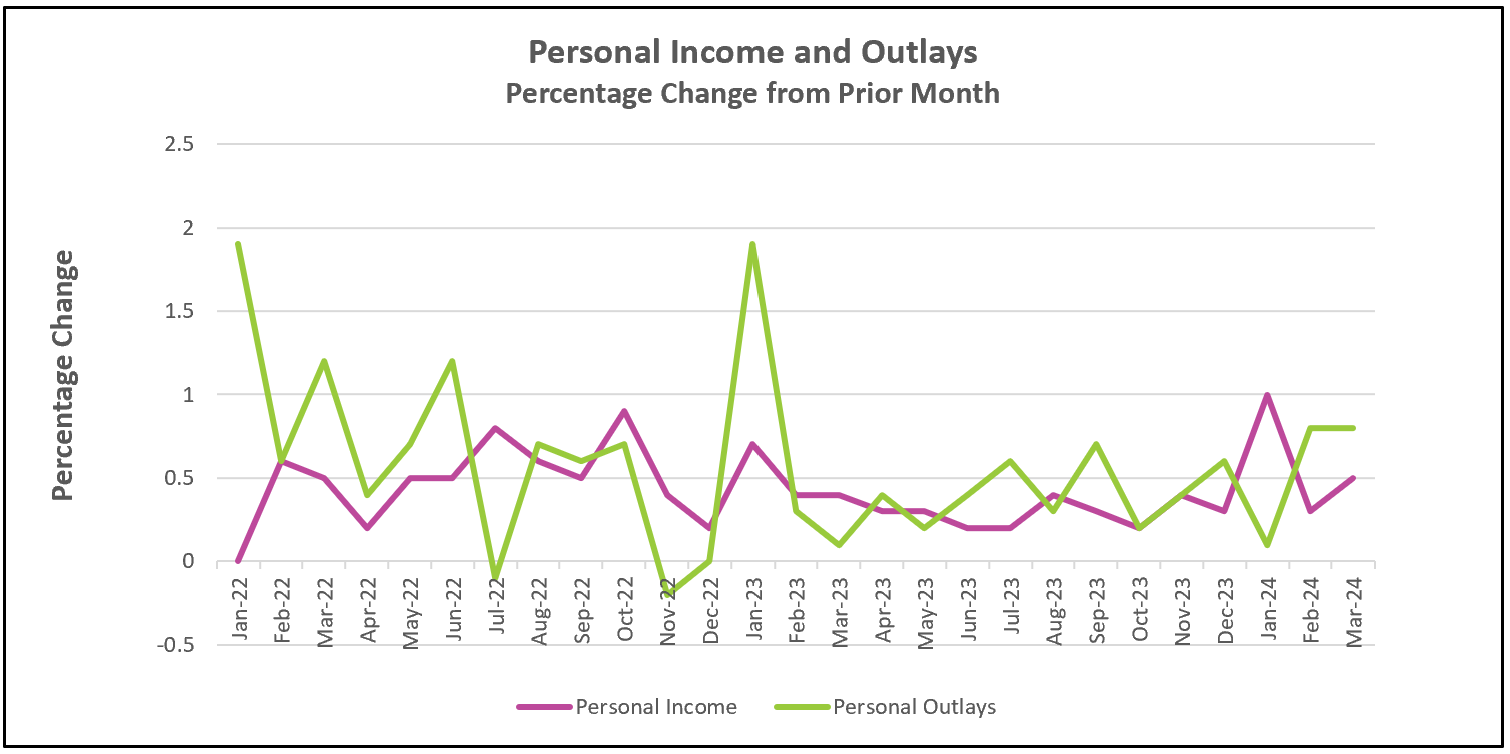

Last Thursday, the commerce department reported moderate growth in the third quarter, but not because of a slowdown in consumer spending. In March, consumer spending surged by 0.8%, matching the previous month’s growth and marking the most substantial increase since January 2023. This growth was widespread, particularly in nondurable goods like gasoline. Durable goods purchases also saw a second consecutive monthly increase after a decline in three of the previous five months. Spending on services also rose, albeit at a more moderate pace compared to recent months. Sustaining increases in consumer spending hinges on income keeping pace unless households opt to reduce savings. In March, the savings rate, measured as a percentage of disposable income, fell to 3.2%, the lowest since October 2022.

Higher incomes have enabled consumers to continue their spending spree. Wages and salaries rose 0.7% in March, matching the year’s largest increase and the most since January 2023. Inflation-adjusted disposable income has increased for much of 2023 and 2024, following a decline in late 2021 and early 2022. Because household income growth has outpaced inflation, it is easier for households to spend without straining their budgets. During March, inflation-adjusted disposable income increased by 0.2%, marking the largest gain in five months.

Higher incomes typically increase the demand for most goods and services, which drives prices higher. The recent moderation in inflation appears to be reversing, with the 12-month all-inclusive index rising for the first time since September 2023. Monthly changes continue to exceed policymakers’ target of a 2% annual rate.

Businesses may hesitate to maintain price stability if consumers persist in spending, especially if higher demands result in shortages. Despite economists’ surprise at the labor market’s resilience and continued growth in consumer spending, there are indications that consumer spending may not continue to grow at its current pace. The savings rate decline, a notable rise in borrowing, and a slight decrease in consumer confidence could constrain spending. Moreover, higher costs for essentials such as housing and energy, both of which have seen significant price increases recently, would also reduce funds available for other purchases.

Policymakers are closely monitoring inflation in the service industries because they greatly influence labor costs. Increases in wages often translate quickly into higher prices for consumers. The PCE index for services, excluding energy and housing, has exceeded or equaled the core index in only two months since January 2023. This report and recent strength in the labor market suggest that Federal Reserve policymakers will refrain from decreasing their target federal funds rate when they meet later this week. In fact, recent data suggest they will postpone any reduction for several more months. Fed decision-makers will closely monitor the April Bureau of Labor Statistics Employment Situation report, scheduled for release on May 3rd, to gauge the labor market’s resilience. A slight cooling in the labor market would be beneficial as it could alleviate inflationary pressures. Following its release, our comprehensive summary and analysis will be accessible on HigherRockEducation.org.