Happy Holidays! October’s Personal Income and Outlays report was full of encouraging news. Inflation subsided slightly. Incomes rose, even after being adjusted for inflation, and Americans continued to spend. News of a coming recession may be premature. However, inflation remains well above an acceptable level, making it very likely that the Federal Reserve will continue to increase interest rates. The jumps in income and outlays pose additional challenges for the central bank by increasing the likelihood that it will take longer for inflation to return to an acceptable level.

The highlights of the Bureau of Economic Analyses’ full report, Personal Income and Outlays - October 2022, are listed below.

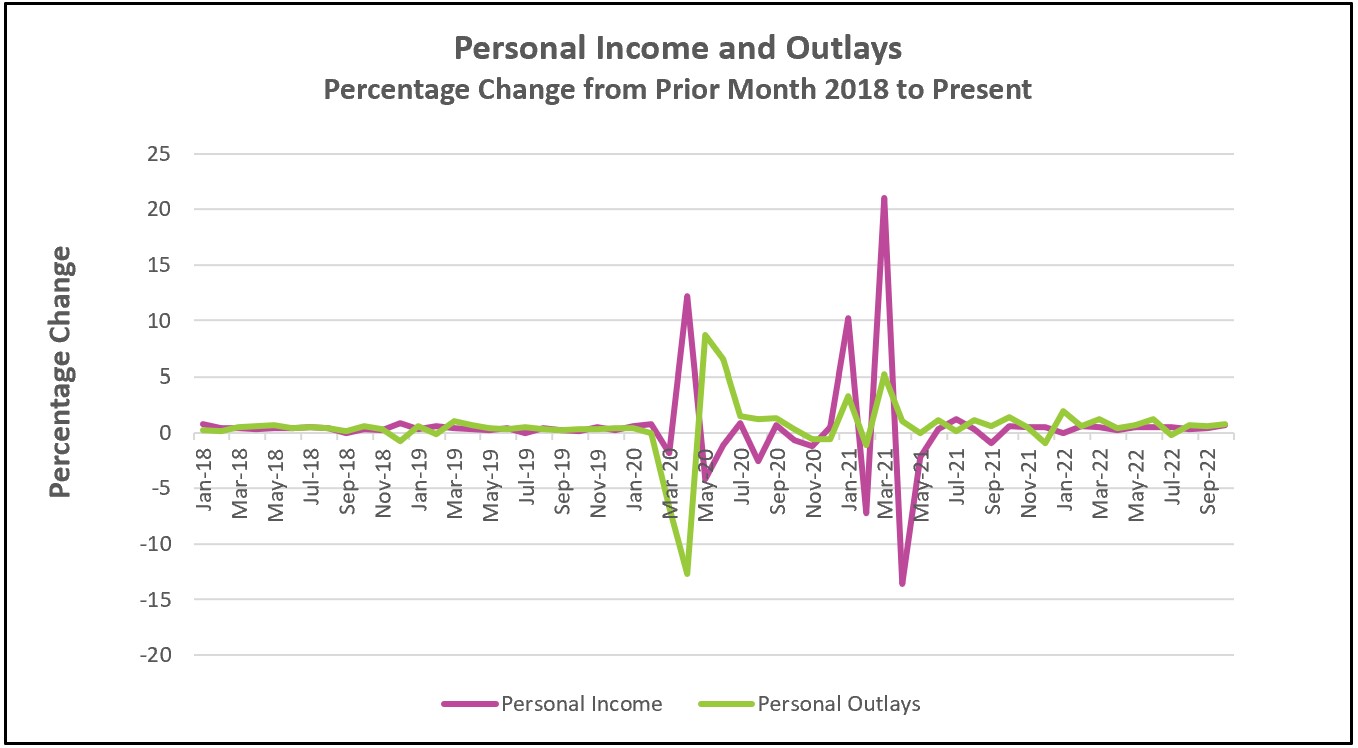

Most economists are surprised by the durability of the US economy. They give credit to consumers who continue to spend. The growth in consumer spending has fueled the economy and has likely prevented (or delayed) a recession. Consumer spending accounts for approximately 70% of economic activity. Personal outlays increased 0.8% in October before adjusting for inflation and 0.5% after adjusting for inflation. October’s increase was the greatest since June, and gains in consumer spending have exceeded increases in disposable income every month since July. After adjusting for inflation, spending on merchandise increased by 1.1% in October. Sales of motor vehicles led the way. A pent-up demand led to increases in the sales of motor vehicles despite escalating prices and higher interest rates. Households continued to increase spending on services, up 0.2% after inflation. Why have consumers been so resilient in the wake of high inflation and higher interest rates?

Income continues to rise: The added number of employees and the real income growth have provided Americans with funds to continue spending. At the end of 2021 and the first half of 2022, disposable income did not keep pace with inflation, so most families lost purchasing power each month. However, disposable income growth exceeded or equaled inflation every month since June. Labor shortages have forced employers to increase wages to attract and retain workers. Real wages increased by 0.2% in October.

Americans are saving less: Americans are dipping into their savings to fund their spending. The savings rate, when measured as a percent of disposable income, has fallen every month since March and reached its lowest rate since July 2005. Some households are strapped for cash and are spending more on necessities because the prices of essentials like food, shelter, and gasoline have increased dramatically. Food prices are 11.6% higher than a year ago, and gasoline prices increased 18.4% over the same period. However, more affluent consumers may be more willing to dip into savings and borrow because they are encouraged by the low unemployment rate and the fact that job openings exceed willing workers. They remain confident that, if necessary, they could find a job quickly.

Use of credit: Americans have used credit. The Federal Reserve reported that the use of revolving credit (credit cards) increased at an annual rate of 12.9% in the third quarter. Nonrevolving credit rose by 4.9%.

Measures of inflation using the personal consumption price index (PCE price index) were less in October. Economists favor the PCE price index because it accounts for changes in how people shop. For example, consumers may switch from a higher-priced national brand to a lower-priced store brand. The PCE index tends to be lower than the more widely published consumer price index, which assumes shopping patterns remain unchanged. (The CPI compares the cost of the same market basket of goods and services.)

While the core inflation rate fell from 5.2% to 5.0%, it remains above the Federal Reserve’s target of 2%. It has also proven challenging to budge and has remained between 4.7% and 5.2% since June. A tight labor market has increased wages, which fuels consumer spending, making it easier for businesses to raise prices and pass through their higher labor costs. This vicious cycle of increasing wages, hiring more workers, and raising prices makes the Fed’s job harder.

Policymakers at the Federal Reserve are expected to be less aggressive but continue to raise rates. Chairman Powell made that clear in a remark earlier this week that “Ongoing increases will be appropriate. We have a long way to go in restoring price stability.” The Fed will likely increase its benchmark by 0.5% when it meets in two weeks after having four successive 0.75% increases. Policymakers hope their rate increases will soften the labor market, deter businesses from expanding, and slow consumer spending – thereby cooling inflation.

Will a tight labor market continue to push incomes higher, making the policymaker’s job to contain inflation more difficult? We will get some inkling of employer sentiment and employment when the Bureau of Labor Statistics releases The Employment Situation – November 2022 on December 2nd. Check back to HigherRockEducation.org for our summary and analysis of this important data.