The Bureau of Economic Analysis Real Gross Domestic Product, 1st Quarter 2026 (Advance Estimate) painted a mixed picture of the US economy during the first quarter. Its key takeaways include:

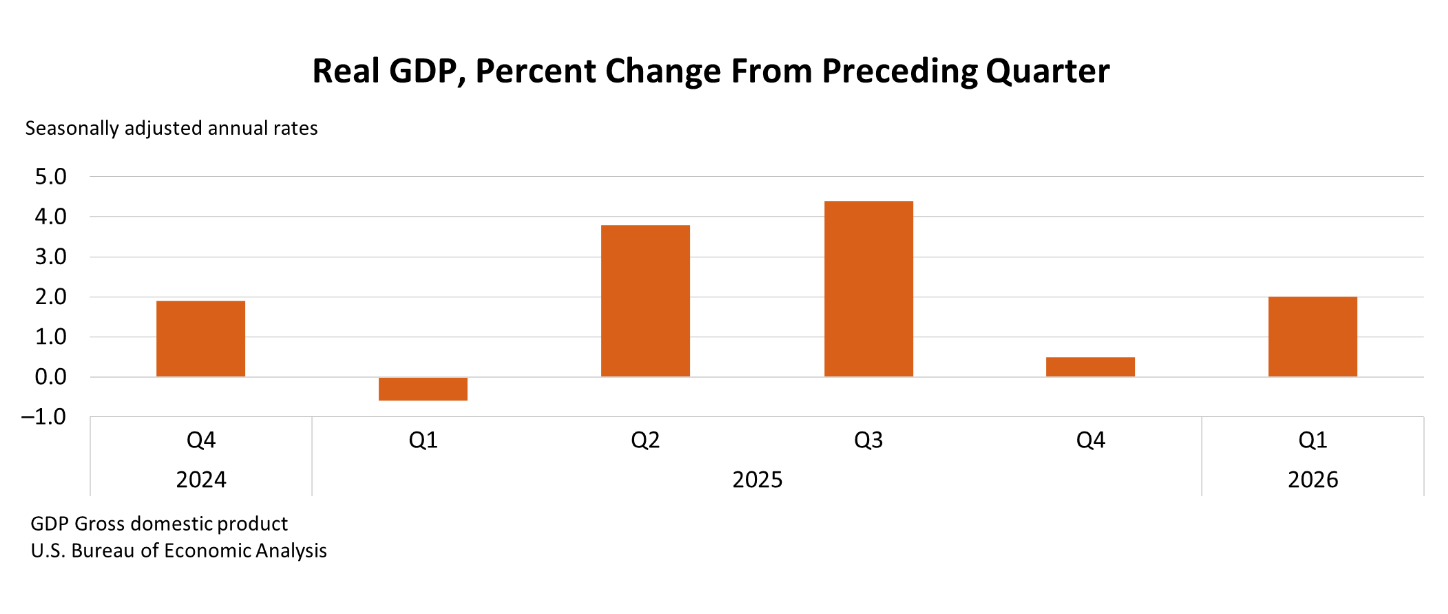

The U.S. economy showed surprising resilience in 2026’s first quarter, expanding at a 2.0% annual rate, up from 1.4% in the final quarter of 2025. Much of that strength, however, came from unusual sources. A surge in business investment—particularly in artificial intelligence (AI)—and a sharp increase in federal government spending following the resolution of the government shutdown were the primary drivers of growth. It is also important to note that much of the first quarter’s activity occurred before February 28th, when the U.S. and Israel launched attacks on Iran, an event that has since added considerable uncertainty to the economic outlook.

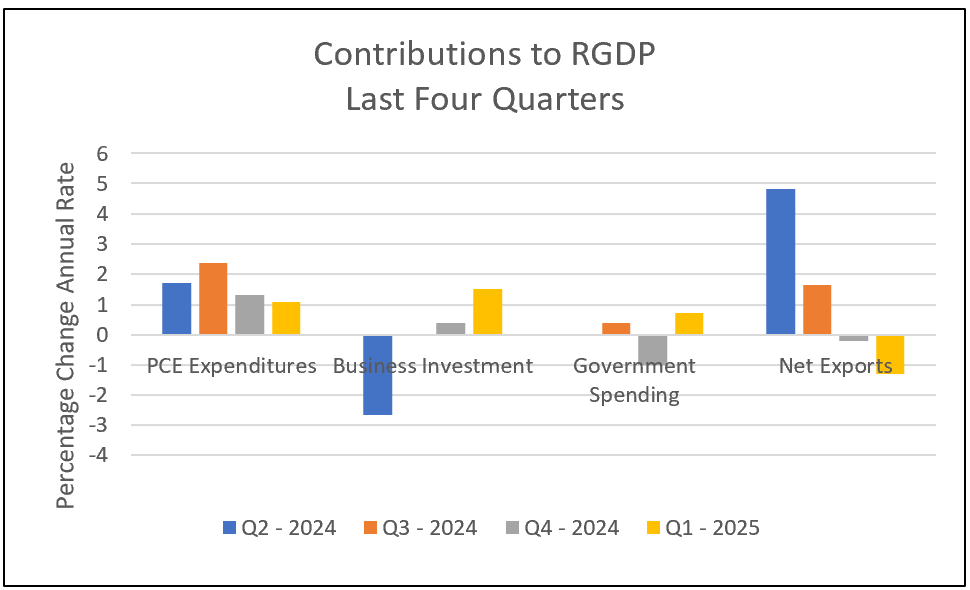

Business investment alone accounted for more than half of the economy’s growth, underscoring how heavily companies are leaning into AI-related spending. Firms are investing aggressively in equipment and technology to remain competitive, and analysts expect that trend to continue through 2026. However, residential investment declined for a fifth consecutive quarter, falling 8%—a clear sign of ongoing weakness in the housing sector.

At the same time, federal government spending rebounded sharply, rising more than 9% and making its largest contribution to growth since the early days of the COVID-19 pandemic. This marked a stark reversal from the previous quarter, when a steep decline in government spending weighed heavily on overall output.

Meanwhile, both imports and exports rose, but faster growth in imports offset the positive contribution from net exports, subtracting from overall RGDP. Economists will be encouraged by a solid 2.5% increase in “real final sales to domestic purchasers,” a figure that looks beyond these volatile components. The increase suggests the economy’s underlying demand remains relatively healthy despite the headline noise.

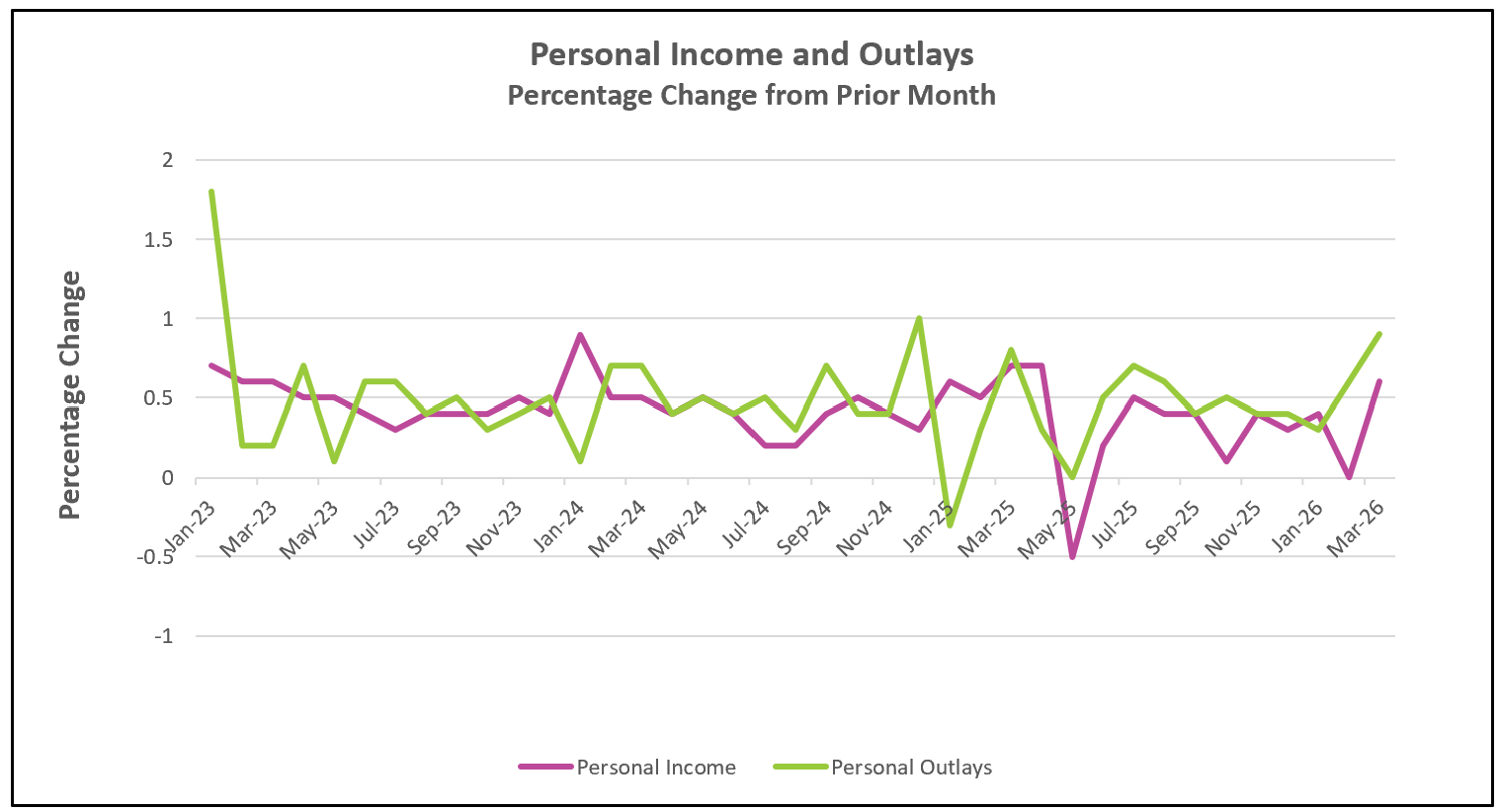

Both personal income and spending rose in March, but the details were less encouraging. Quarterly consumer spending increased at just a 1.6% annual rate, the slowest pace in a year. Gains were concentrated in services such as health care and financial services, while goods spending stalled. Given that consumer activity accounts for roughly 70% of economic output, even a modest slowdown can have significant consequences. When households begin to pull back, it often reflects growing caution and can ripple across the broader economy.

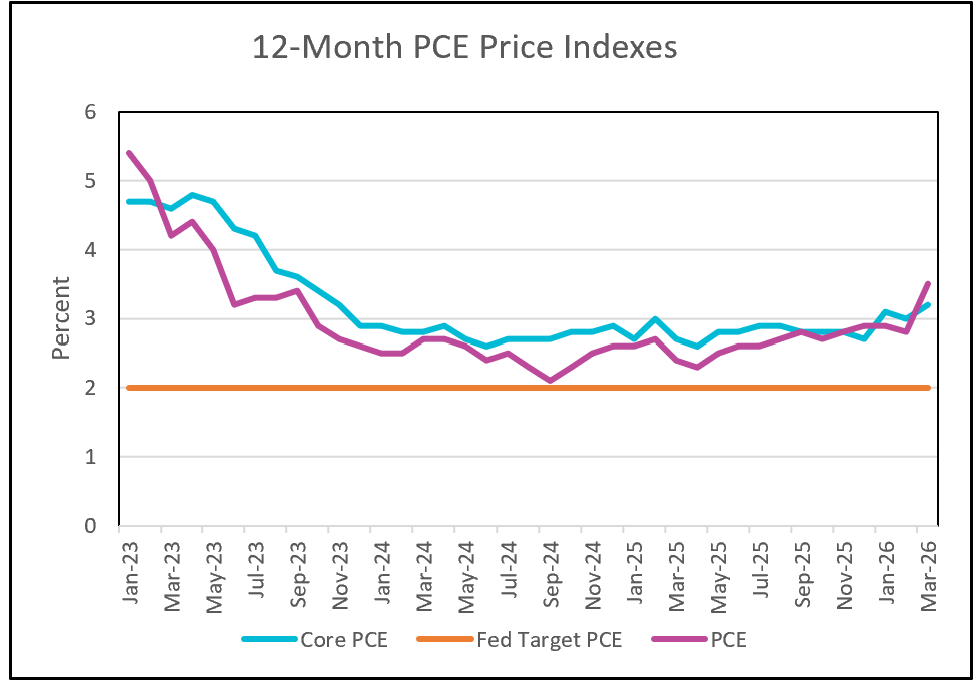

Adding to these concerns, income growth is failing to keep pace with inflation. Personal income rose 0.6% in March, while inflation—as measured by the personal consumption expenditures price index—increased 0.7%, eroding consumers’ purchasing power. This dynamic is particularly troubling amid a sharp rise in energy costs. According to AAA, gasoline prices have surged to nearly $4.50 per gallon, up from $2.98 before the conflict began. Higher fuel costs act like a tax on consumers, diverting money away from discretionary spending and likely contributing to the recent slowdown.

The Federal Reserve remains in a difficult position. Policymakers held interest rates steady at their most recent meeting, as inflation continues to run well above the Fed’s 2% target and shows signs of accelerating. With inflation pressures persisting and growth increasingly uneven, the Fed must balance the risk of tightening too much against the danger of allowing inflation to become entrenched.

Looking ahead, significant economic risks remain. The geopolitical backdrop has become more fragile, particularly amid the Strait of Hormuz blockade, which is disrupting global energy supplies. This has contributed to rising prices, increased volatility, and heightened uncertainty across global markets. While business investment and government spending have provided a near-term boost, a cautious consumer and mounting external risks suggest the road ahead may be far less stable. An increase in the unemployment rate and a slowdown in hiring could further dampen consumer sentiment, ultimately slowing spending and RGDP growth.

Economists should gain insights into the economy’s health when the BLS publishes two economic releases scheduled for the next two weeks. April’s Employment Summary will provide insights into the labor market’s health when released on May 8th. In addition, on May 12th, April’s CPI will be released, providing insights into the severity of the impact of the war with Iran on prices. HRE will provide a summary and its analysis shortly after each of these reports is released.