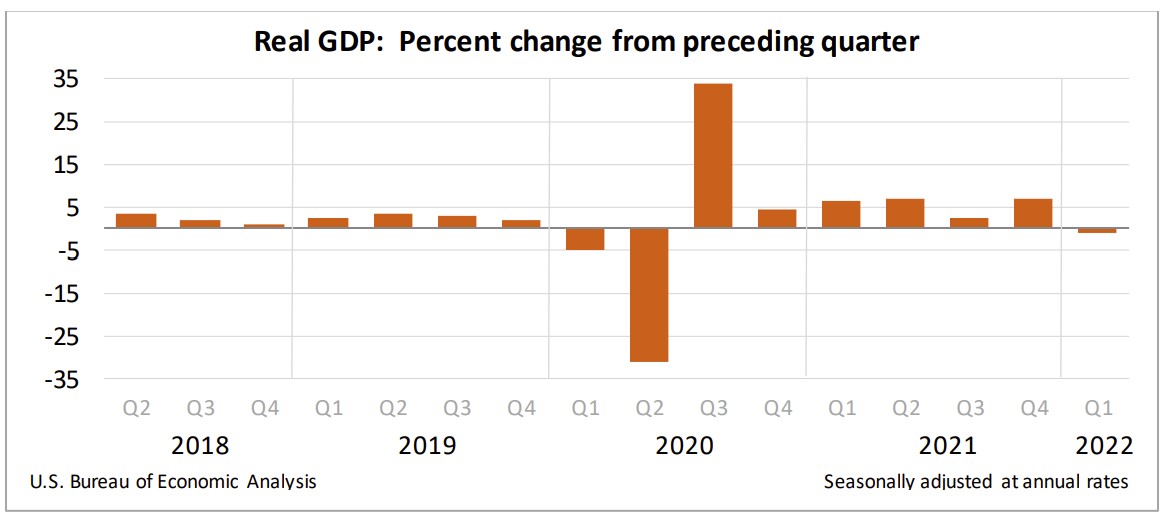

The US economy contracted 1.4% in the first quarter after increasing 6.9% in the fourth quarter of 2020. Does the dramatic change signal a recession? A decrease in net exports, inventories, and government spending pushed the US real gross domestic product (RGDP) lower for the first time since the second quarter of 2020. Trade and inventories are the more volatile components of GDP and probably are not indicative of a continuing trend. Consumer and business investments are more stable and gained in the first quarter, suggesting an underlying strength and improbability that another recession is beginning.

Readers can access the Bureau of Economic Analysis’s news release at Gross Domestic Product, First Quarter 2022 (Advance Estimate). Here are the report’s highlights.

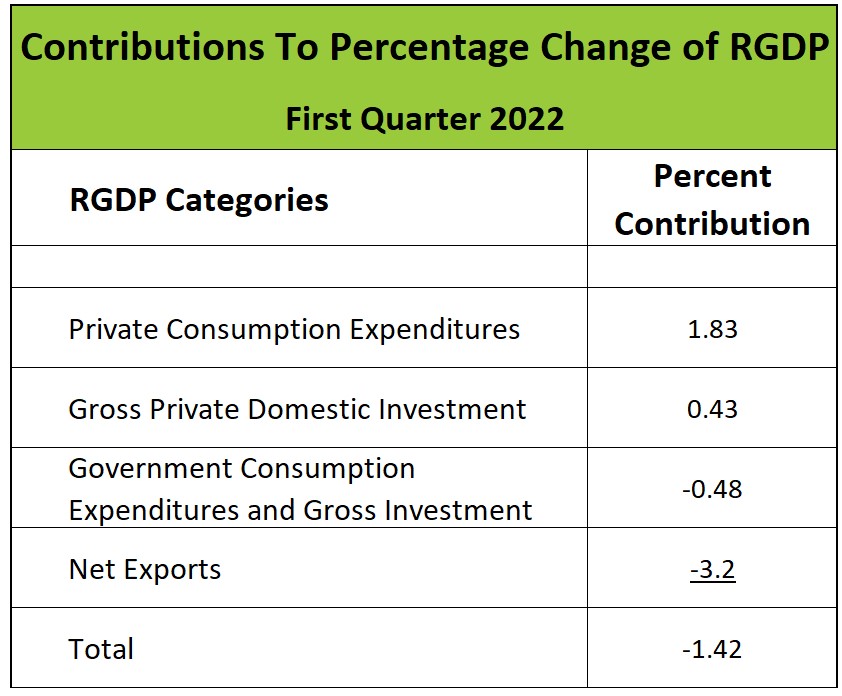

Gross domestic product is the sum of personal consumption expenditures (consumer spending), private domestic business investment, government consumption and investments, and net exports. The table below summarizes the contribution of each category to the quarterly change in RGDP.

Source: BEA Table 2 Contributions to Percent Change in RGDP

Personal Consumption Expenditures: Consumer spending continues to be the most resilient component of the US economy. It is also the most crucial factor because it comprises approximately 70% of the economy. In the first quarter, consumer spending rose 2.3% and contributed 1.8% to the change in GDP. It has increased every quarter since the second quarter of 2020. Gains were the largest in the service sector because people returned to leisure activities outside their homes.Inflation threatens continued growth in consumer spending. Real disposable income decreased for the fourth consecutive quarter, making it increasingly difficult for households to continue spending. Earlier this month, the Bureau of Labor Statistics reported that the consumer price index rose at an annual rate of 8.5%, while average hourly earnings only increased 5.6%. Fortunately, most households have adequate savings and low debt, which enable them to continue spending, but families will eventually cut back if the trend continues.

Gross Private Domestic Investment: Business investment gained 2.3%. Equipment sales grew over 15%, and residential investment rose 2.1%. Businesses invested heavily in equipment and intellectual properties, but companies were slow to replenish their inventories, thereby pushing total investment down to 2.3%. The decline in inventories reduced the first quarter's RGDP by 0.84%. But this change is not surprising since businesses dramatically increased their inventories in the fourth quarter to protect themselves from disruptions in the supply chain. By comparison, an increase in inventories added 5.3% to the fourth quarter’s RGDP. Inventories will likely grow in the second quarter as current inventories are depleted.

Government: Government consumption and investment expenditures fell 2.7% and contributed 0.43% to the contraction in RGDP during the first quarter. Spending on the national defense fell by 8.5%.

Net Exports: The trade deficit widened as exports fell and imports increased. GDP does not include imports since they are not produced domestically. The US economy recovered faster than most other countries, which increased the demand for imports relative to exports. This trend will likely continue. The Ukraine – Russia war will adversely impact trade by weakening many European economies and strengthening the US dollar. A stronger dollar reduces exports because American goods and services become more expensive in the receiving country while making imports cheaper in the United States.

Most economists predict the economy will grow in the second quarter. The economic fundamentals remain strong. The US economy has never progressed into a recession when the unemployment rate is falling and profits are rising. Last month, the Bureau of Labor Statistics reported that unemployment fell to 3.6%, close to the historically low rate of 3.5% before the pandemic. Business profits are increasing. The BEA reported that profits increased 21.0% during the fourth quarter of 2021. Most financial analysts expect earnings to continue to rise in 2022. The BEA will release first-quarter profits in its May 26th GDP report. Consumer spending continues to increase, and households are in a stronger financial position than before the pandemic. The enormous bounty consumers received from the government during the COVID pandemic bolstered their savings and enabled many families to pay down their debts.

But most analysts have lowered their growth projection for 2022. Many threats to the US economy remain. COVID continues to impact the supply chain and reduce China’s demand for US goods and services. Shutdown measures continue to aggravate the supply chain by delaying shipments of many finished goods and parts.

Inflation is the main threat. A surging demand and supply challenges pushed prices up before Russia invaded Ukraine. The war has only exacerbated inflation. Cutbacks in gasoline and natural gas production have pushed up energy prices globally. Food prices have escalated because of wheat, corn, and other grains shortages, of which Russia and Ukraine are significant suppliers. The Federal Reserve clearly stated its intention to raise rates to combat inflation following its last meeting. It is improbable that the BEA's report will change its strategy of increasing rates by one-half percent when policymakers meet next week. Higher rates ease inflation by decreasing spending. For example, higher mortgage rates will lessen the demand for homes and other amenities associated with a new home, such as furniture and appliances.

The BEA will release Personal Inflows and Outflows for March on April 29th. It will provide valuable insights into the strength of consumer spending, whether income gains continue to be less than inflation, and the impact of the war on prices and trade. Check back to HigherRockEducation.org shortly after its release for our summary and analysis.