State of The Economy - December 2018

In 2018, economic growth surged in the US, unemployment fell to near record lows, without a significant jump in inflation. I confess to being surprised that inflation wasn't higher. Normally when growth stretches beyond its

full employment output the economy becomes overheated and inflation follows. (Most economists believe the full employment rate is between 4 and 5 percent.) Figures highlighted in each report and a graph are furnished. My analysis and summary are provided at the end of the blog.

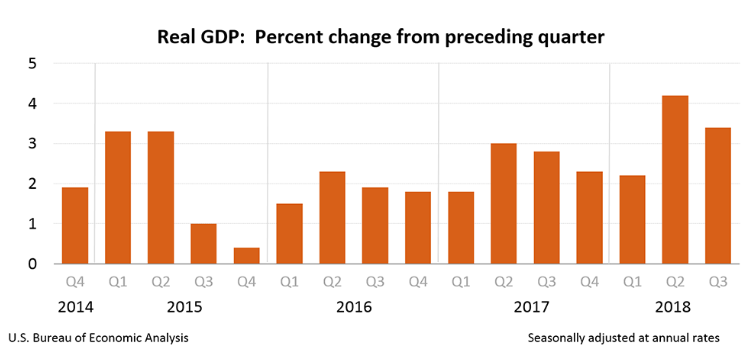

Real Gross Domestic Product

The Bureau of Economic Analysis (BEA) released its “third estimate” for the third quarter of 2018 on December 21st. (

Gross Domestic Product, Third Quarter Estimate) Few adjustments were made from last month’s second estimate. Here are the highlights:

- The third estimate was revised downward 0.1%. Growth in the real gross domestic product (RGDP) grew 3.4%, which is 0.8% lower than the second quarter's 4.2% growth rate.

- Inflation, as measured by the PCE price index, was revised upward from 1.5% last month to 1.6%. But this remains lower than the 2.0% rate recorded in the second quarter. Core prices increased 1.6%.

- Federal government spending increased 3.5%. This is down from a growth rate of 3.7% in the second quarter, but remains relatively high. Federal spending has not increased more than 3% in consecutive quarters since the first and second quarters in 2010.

- Exports fell 4.9% after increasing 9.3% in the second quarter.

- Corporate profits increased $78.2 billion in the third quarter. This compares to an increase of $64 billion In the second quarter.

- The BEA's advanced estimate for the fourth quarter of 2018 is scheduled to be released January 30th.

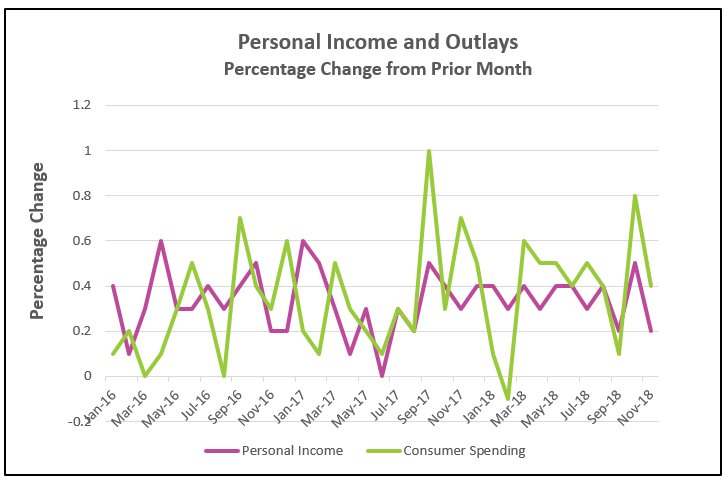

Personal Income and Outlays

In October and November consumer spending increased substantially, but the growth in personal income did not keep pace. Here are the figures that highlight the BEA’s

Personal Income and Outlays, November 2018 report published on December 21st.

- Personal income increased 0.2% in November. This is down from an increase of 0.5% in October and matches the slowest pace in 2018. (September also increased 0.2%.) This follows October’s large increase that was the largest since February 2017.

- Disposable, or after-tax income, also increased 0.2% in November.

- Consumer spending remains strong, although it slowed in November. Spending increased 0.4% in November, down from a 0.8% increase in October. (October’s figure was revised upward from 0.6%.)

- Savings as a percent of disposable income continued to decrease to its lowest rate since March 2013.

- November's PCE price index increased 0.1%, while the core price index, which excludes volatile food and energy prices, only increased 0.1%. The PCE price index rose 1.8% when measured over the past 12 months. The core prices rose 1.9%. Both remain below the Federal Reserve's target of 2.0%.

- December’s Personal Income and Outlays report is scheduled to be released January 31st.

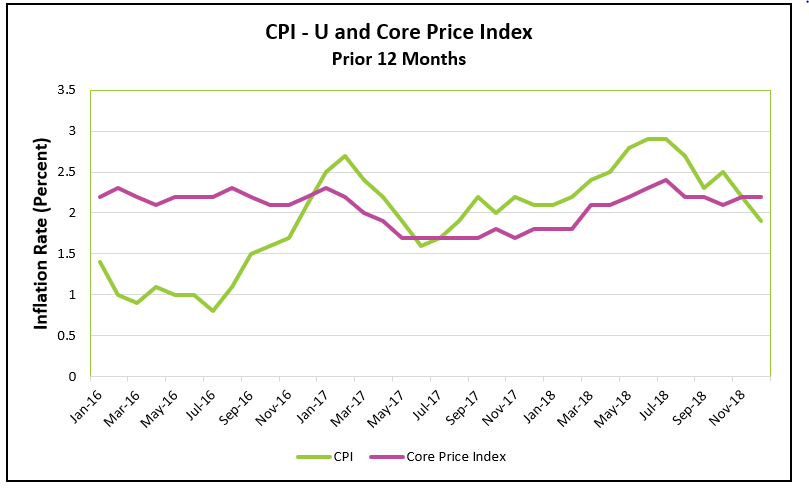

Consumer Price Index

The price index was lower in December, largely because of falling energy prices. The Bureau of Labor Statistics published

Consumer Price Index – December 2018 on January 11th. Here are the highlights:

- The CPI decreased 0.1% in December - the first decrease since March. Prices rose 1.9% over the prior 12 months.

- The core price index rose 0.2% in December and 2.2% over the prior 12 months.

- Gasoline prices fell 7.5% in December, which is the main reason the core index is higher than the CPI.

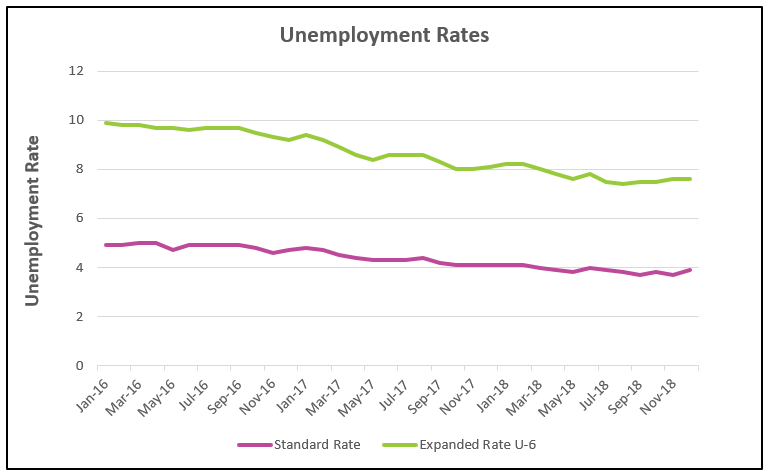

Employment

On January 4th the BLS published its December employment report. The full report can be read by going to

The Employment Situation – December 2018. Here are the highlights:

- The standard unemployment rate increased from 3.7% in November to 3.9% in December.

- 312,000 workers were added to payrolls in December and a total of 2.64 million during 2018.

- The average hourly wage for all employees on private non-farm payrolls increased $0.11 to $27.48. This is a 3.2% increase, which is the largest gain since 2009.

- The average workweek increased 0.1 hour to 34.5 hours.

- U-6, the broader measure of unemployment, remained at 7.6%.

Summary and Analysis

The Bureau of Labor Statistic’s most recent employment report was outstanding, even though unemployment increased from 3.7% to 3.9%. 312,000 workers were added to non-farm payrolls in December. Many formerly discouraged and long-term unemployed returned to work. There were 99,000 fewer discouraged workers at the end of 2018 than at the end of 2017. The labor participation rate increased 0.4% during 2018. It ended the year at 63.1%. Shortages of labor has induced employers to increase wages. Real wages increased 1.1% in 2018, which means most households are seeing an improvement in their buying power.

Gas prices were 7.5% lower in December, which contributed greatly to the 0.1% drop in December’s consumer price index. More people working, higher wages, and lower gasoline prices result in more money in people’s pockets. It is not surprising that PCE increased in recent months (0.8% in October and 0.4% in November). Continued strength in consumer spending is essential to maintaining economic growth because it accounts for approximately two-thirds of economic activity, and other areas of the economy have shown some weakness. Exports fell 4.9% in the third quarter. Tariffs combined with weaker global economies have reduced the demand for exports. Federal government spending increased 3.5% in the third quarter, but a prolonged government shutdown would affect government expenditures and consumer spending. Many government employees and government subcontractors will need to find ways to spend less, at least until the shutdown is over. At that time their spending will resume, but some expenditures, such as going out for a meal or movie, will never be made.

Last month the

FOMC raised the target federal funds rate to between 2.25% and 2.5%. This was the fourth increase in 2018. The consensus is there will only be two increases in 2019. Next month the BEA will publish its advance estimate of growth in the fourth quarter. I am confident it will confirm that growth exceeded President Trump’s goal of 3% in 2018. I share most economists’ views that next year the economy will set a record for the longest recorded expansion, but the pace of growth will slow. How long will this expansion last? After all, economies are cyclical, and a downturn is coming. While the US economy remains healthy, there are a few signs that we are nearing this recovery’s end. A prolonged government shutdown and continuing trade disputes will impact the first quarter of 2019. Housing was down 3.6% in the third quarter and could be hampered in the future by higher interest rates. Finally, the US economy remains tied to world economies and at some point, if the major world economies continue to struggle, the US economy would be impacted, even if trade disputes are resolved.