While inflation raged for the past year, consumers spent, and incomes rose – until December. In December, inflation eased for the third straight month. Households drew in their purse strings and spent less and saved more. Incomes also rose at a slower pace. This report provides the policymakers at the Federal Reserve with encouraging news before they meet later this week to decide their strategy for moving forward.

The highlights of the Bureau of Economic Analyses’ full report, Personal Income and Outlays - December 2022 are listed below.

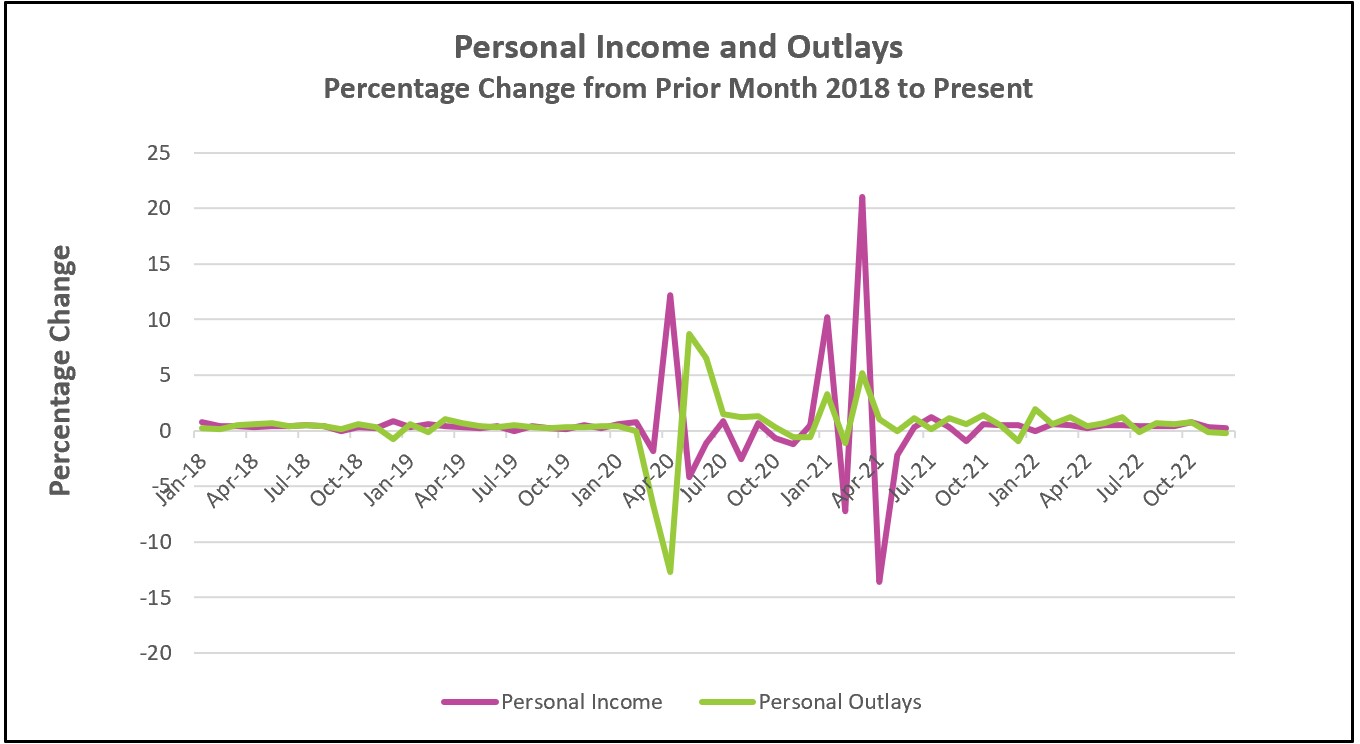

Policymakers at the Federal Reserve will be very encouraged by this report. Price increases have moderated after almost a year of aggressively combatting inflation by raising its benchmark rate seven times from near zero to over four percent. Their objective was to slow the growth of the economy’s aggregate demand. Americans spent 1.6% less on goods in January than in December. Sales of services increased in January, but the pace has slowed. In January, service purchases increased by 0.5%, down from 1.2% as recently as August.

Last week the BEA reported that growth of the economy’s real gross domestic product slowed from an annual rate of 3.2% in the third quarter to 2.9% in the fourth quarter. Much of the growth resulted from volatile components such as growth in inventories, net exports, and government spending. Economists gain a better insight into the private domestic aggregate demand by using the ratio of final sales to private domestic purchases, which strips out government and the more volatile components of GDP. The ratio only increased by 0.2% in the fourth quarter, the smallest increase in more than two years.

The PCE price index receives less publicity than the CPI, but it is probably the more important measure of inflation. The PCE is more influential than the CPI in far-reaching economic policy decisions because it is preferred by the Federal Reserve when determining its monetary policy. Economists also prefer using the core index when evaluating trends. January’s core fell to 4.4%. It reached 5.2% in February 2022. The index remains significantly above the Federal Reserve’s 2% target, making it very likely that policymakers will continue tightening when it meets later this week. They also want more evidence that wage increases are subsiding—higher wages pressure businesses to increase their prices to maintain their profit margins.

Will a tight labor market continue to push incomes higher, making the policymaker’s job to contain inflation more difficult? We will learn more when the Bureau of Labor Statistics releases The Employment Situation – January 2023 on Friday, February 3rd. Check back to HigherRockEducation.org for our summary and analysis of this important data.