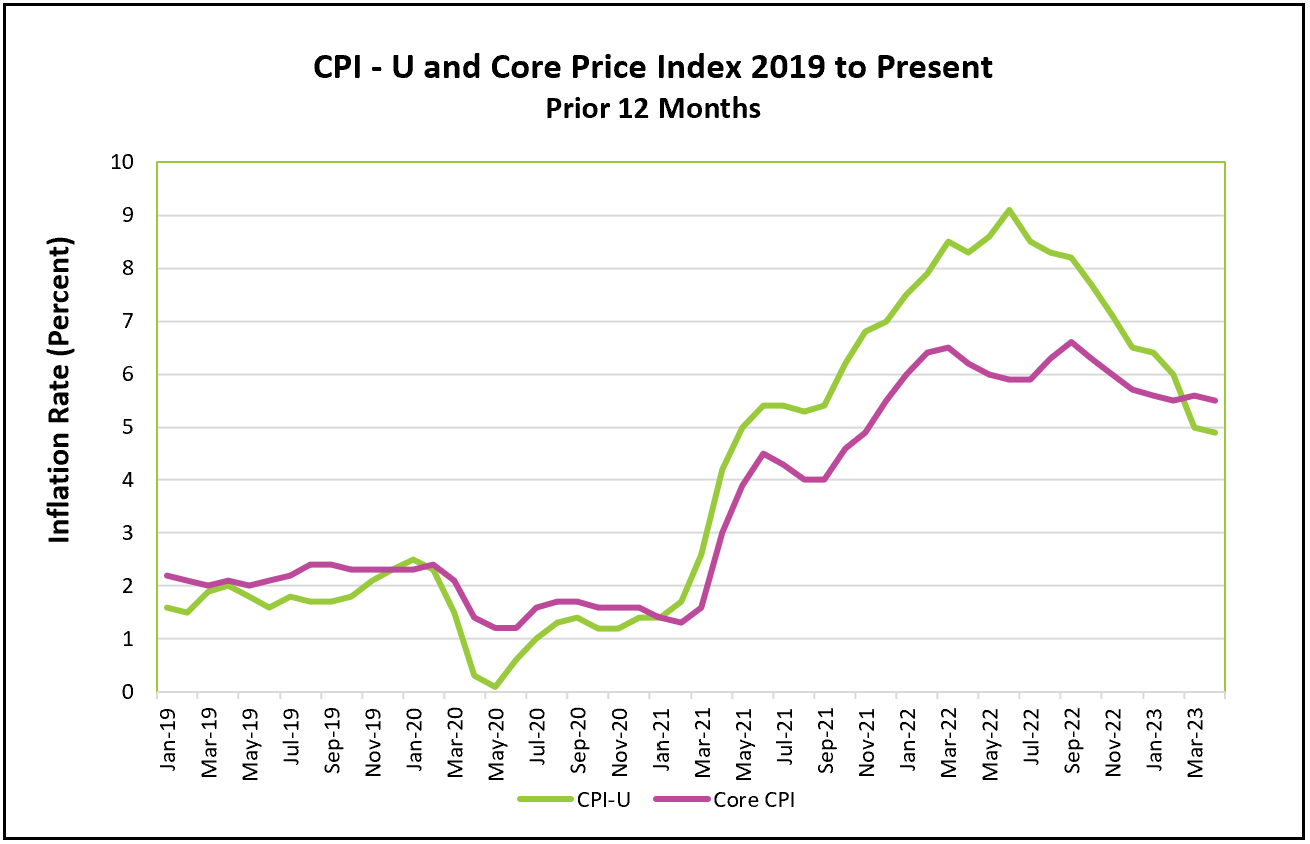

Prices rose in April. Higher housing, gas, and used-car prices were the largest contributors. Monthly price changes have been choppy. The rolling three-month average reached a low of 0.27% in January, only to increase in February and March. Economists prefer measuring inflation over the 12 prior months because it reveals trends. The CPI rose 4.9%, down from its peak of 9.1% in June 2022, the smallest increase in two years. The slight drop in the 12-month index combined with a monthly CPI increase suggests the return to the Federal Reserve’s target of 2% inflation will be long and choppy.

The highlights and analysis of the Bureau of Labor Statistics press release, Consumer Price Index – April 2023, are summarized below.

Lower grocery prices provided relief to everyone and helped lower the inflation rate. Grocery prices eased 0.2%, but the cost of dining out rose 0.4%, leaving the overall food index unchanged from March. Energy prices rose 0.6%, even after a 3% surge in gasoline prices. Lower fuel oil and natural gas prices restrained the energy increase.

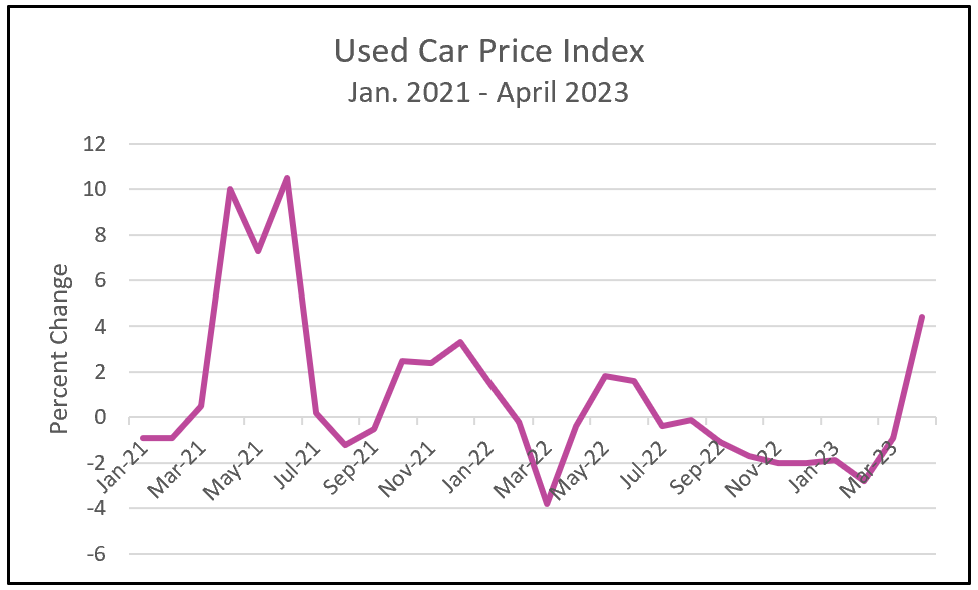

Used-car prices surged 4.4% in April, rising for the first month since June 2022. The increase was second only to shelter prices in influencing the rise in April’s CPI. Used-car prices skyrocketed early in the pandemic when a chip shortage and factory shutdowns caused a shortage of new cars. But prices began to fall when producers resolved most of their supply challenges, and new cars became available. Pent-up demand and continuing chip shortages caused manufacturers to ration their chip supplies, reserving them for the most profitable vehicles and cutting back on less expensive options. Meanwhile, higher interest rates have increased the cost of owning a car. A used car is the only affordable option for a larger portion of the population than just a few months ago.

Economists prefer using a core price index when evaluating trends because the core index excludes volatile food and energy prices. The core index has been slower to fall than the CPI, primarily because shelter prices continue to increase at a fast pace. However, economists expect the shelter index to lose momentum. There is evidence rents have increased at a slower rate in recent months.

Policymakers at the Federal Reserve have increased their benchmark rate to the highest level in sixteen years. Early in the pandemic, households were flush with cash and willing to spend. The economy’s aggregate demand was increasing too rapidly – causing demand-pull inflation. Inflation was magnified when supply constraints prevented suppliers from meeting the growing demand for their goods and services. Production costs escalated as suppliers had to pay premiums for materials and delivery. The economy’s aggregate supply fell, causing cost-push inflation. The economy’s resources did not keep up with the growing demand. Businesses responded by increasing their prices.

Most of the supply constraints have improved, but a shortage of workers remains many companies’ most significant challenge. Job openings continue to exceed available workers by almost two to one. Employers have increased wages to attract and retain workers. The higher wages have helped fuel the growth of consumer spending. Economists are paying close attention to the prices of services because labor is frequently the largest expense of service providers. As long as a worker shortage continues, wages will increase and push prices higher.

Three large banks failed in the last three months. Higher interest rates reduced the value of their holdings, which ultimately depleted their reserves after large bank runs. The economy had not digested the total impact of the bank failures when this month’s data were gathered. Some banks may consider themselves vulnerable and increase their reserves by curtailing lending, further slowing the economy.

Also looming is a possible debt crisis. Potential Congressional inaction from a prolonged battle to increase the debt ceiling could also push the economy into a recession. Default on the federal debt (which has never happened in the United States) would push interest rates higher and possibly cause a global financial crisis.

Federal Reserve Chairman, Jerome Powell, suggested that policymakers will not increase their benchmark rate when they meet in June. A pause will provide time to assess the impact of past rate increases and bank failures. Several government releases, including May’s CPI report, information on the state of the labor market and consumer spending, and a reading of their preferred inflation index, the personal consumption expenditures (PCE) index, will be released before the Fed’s next meeting. On May 26th, the BEA will release Personal Income and Outlays – April 2023, which will provide April’s PCE price index and the direction of consumer spending. Check back with HigherRockEducation.org shortly after its release for our summary and analysis.