Key takeaways from the Bureau of Labor Statistics (BLS) report, The Employment Situation – April 2026, include:

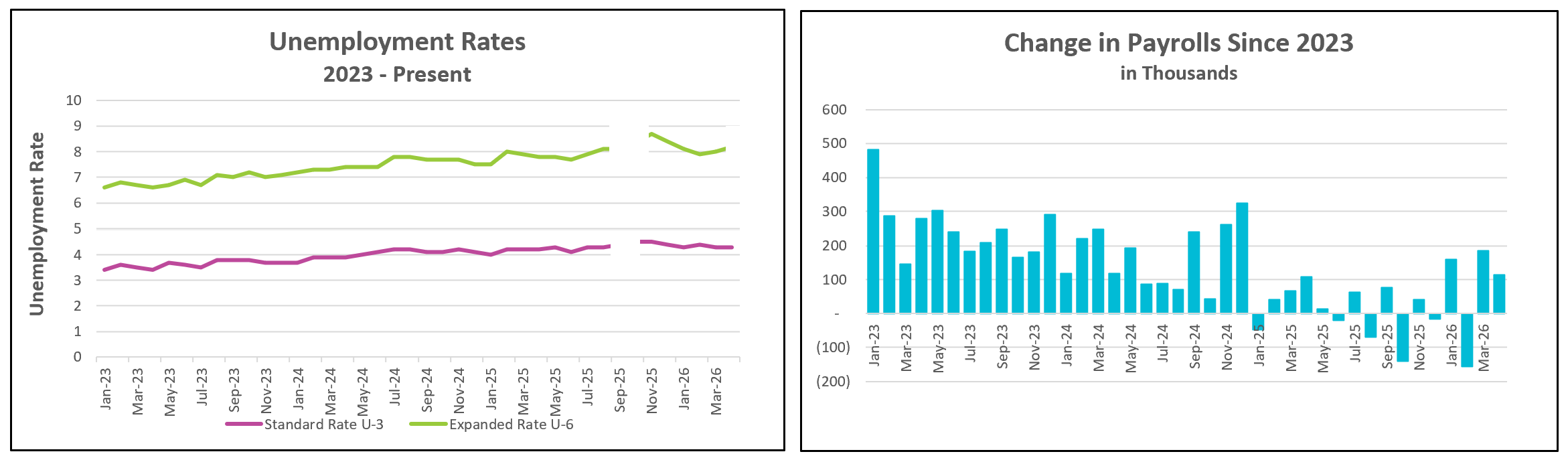

The labor market showed surprising resilience in April as hiring continued to strengthen despite mounting economic and geopolitical uncertainty. Employers added jobs at a faster pace than they did last year, with payroll growth averaging 76,000 per month during the first four months of 2026 compared to just 9,700 per month during 2025. April also marked the first time since the end of 2024 that job gains exceeded 100,000 in two consecutive months, suggesting that hiring momentum has improved. This strength is particularly notable given the supply disruptions and surging oil prices caused by the escalation of fighting with Iran and the closing of the Strait of Hormuz, both of which have placed significant hardship on businesses and consumers alike.

At first glance, the employment picture appears stable, as the unemployment rate remained unchanged at 4.3%. However, a closer look reveals some softening beneath the surface. When rounded to the nearest hundredth, the unemployment rate rose from 4.26% in March to 4.34% in April. The headline figure was also supported by a decline in labor force participation, which fell to its lowest level since October 2021. In addition, 226,000 fewer people were employed in April than in March. These figures suggest that the stable unemployment rate partly reflects fewer people participating in the workforce rather than stronger employment conditions.

Additional warning signs emerged in broader measures of labor market health. The number of people working part-time who wanted full-time work surged by 445,000, helping push the broader U-6 unemployment rate to 8.2%, its highest level of 2026. This increase indicates that while many workers remain employed, a growing number are struggling to secure the hours they need, often an early signal of labor market weakness.

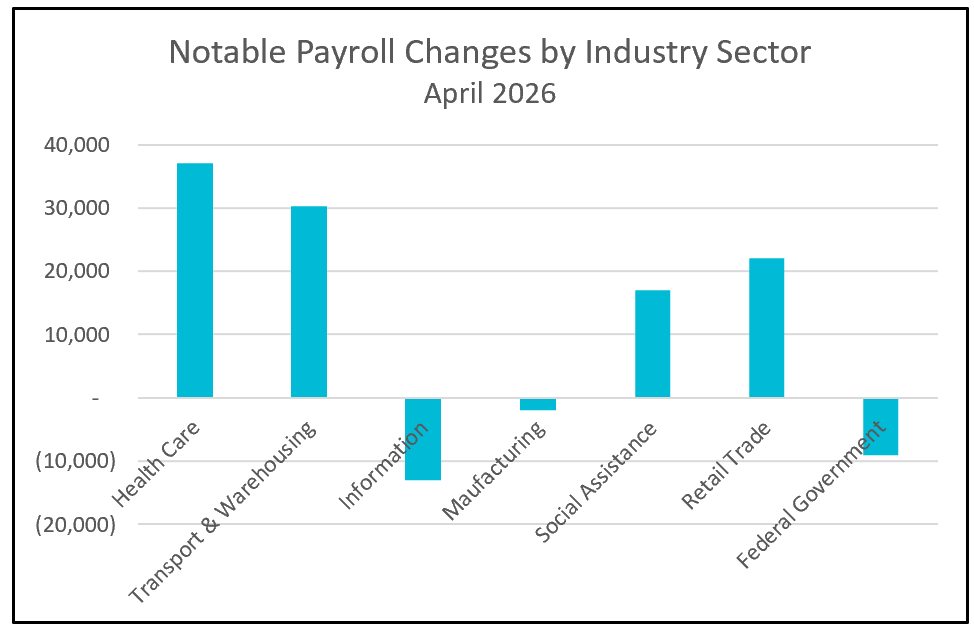

Economists have been encouraged that hiring in early 2026 has been more broadly distributed than in 2025, when most sectors shed jobs and health care and social services accounted for nearly all net job creation. Health care and social services continued to lead the way in April, adding 53,900 jobs. However, April also saw a notable gain of 30,000 jobs in transportation and warehousing. Most of that increase was among couriers and messengers. Since the sector remains roughly 105,000 jobs below its February 2025 peak, this is likely to be a temporary rebound or catch-up from prior weakness rather than the beginning of sustained growth. Other sectors that saw an increase in payrolls included retail (22,000), construction (9,000), and leisure and hospitality (14,000).

Elsewhere, manufacturing remained under pressure, losing 2,000 jobs in April and standing 66,000 jobs below year-ago levels. Federal employment declined by another 9,000 payrolls, bringing total federal job losses since October 2025 to 348,000. Employment in information technology continued to weaken, falling by 13,000, as companies increasingly adopt AI and automation to streamline operations and reduce staffing needs in areas such as programming, IT support, and data analysis.

Households may soon face increasing financial strain if wage growth continues to keep pace with inflation. Average hourly earnings rose just 0.2% in April, well below the 0.6% increase in consumer prices. Consumer spending has remained resilient in part because of large tax refund checks, but once that temporary boost fades, weaker real wages could create significant headwinds for an economy that depends heavily on consumer spending for growth.

This stronger-than-expected employment report is also likely to influence monetary policy. The Federal Reserve will probably view continued job growth as a reason to continue its pause of interest rate cuts. Policymakers have become increasingly concerned by inflationary pressures stemming from higher energy prices and supply disruptions, rather than a weakening labor market.

The largest uncertainty facing the labor market is whether it can maintain its momentum if the conflict with Iran persists. Prolonged hostilities would likely keep energy prices elevated, squeezing household budgets and reducing disposable income. As consumers pull back on spending, aggregate demand would weaken, prompting businesses to slow hiring or reduce payrolls, thereby pushing unemployment higher.

That concern is already reflected in consumer sentiment, which fell to a new low in April, according to the University of Michigan’s widely published consumer sentiment index. Consumer sentiment is often a leading indicator of economic performance, as declining confidence frequently precedes weaker spending and slower hiring. If households become more cautious and businesses respond by scaling back expansion plans, the labor market’s recent gains could prove short-lived. For now, April’s report reflects resilience, but significant risks remain on the horizon. The BLS released April’s consumer price index on Tuesday. It surged to 0.6%. Higher Rock Education will post its analysis and summary soon.