Key takeaways from the Bureau of Labor Statistics (BLS) report, “The Employment Situation – March 2026,” are as follows:

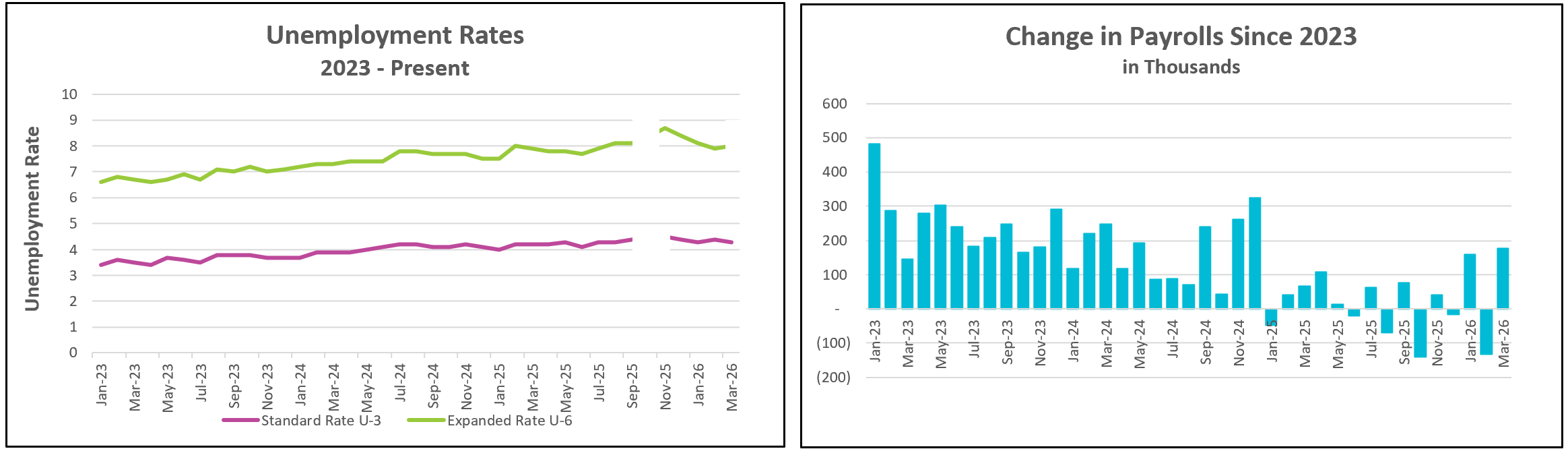

The March employment summary delivered encouraging headline news: job growth rebounded strongly from February, and the unemployment rate declined. Payrolls posted their largest gain since late 2024, suggesting renewed momentum and resilience in hiring. Some of these improvements, however, likely reflect temporary factors rather than a fundamental strengthening of the economy. A significant portion of the job gains came from roughly 31,000 nurses returning to work after a strike in California and Hawaii ended. At the same time, milder weather also allowed more workers—particularly in construction—to return to job sites after February’s disruptions.

Despite the upbeat news, several underlying indicators point to a more fragile economic picture. The unemployment rate fell to 4.3%, but largely because people exited the labor force rather than finding jobs. In fact, the labor force shrank by 396,000, and the number of employed individuals declined as well. A broader unemployment rate (U6) that measures labor underutilization, including discouraged workers and those working part-time for economic reasons, rose to 8%.

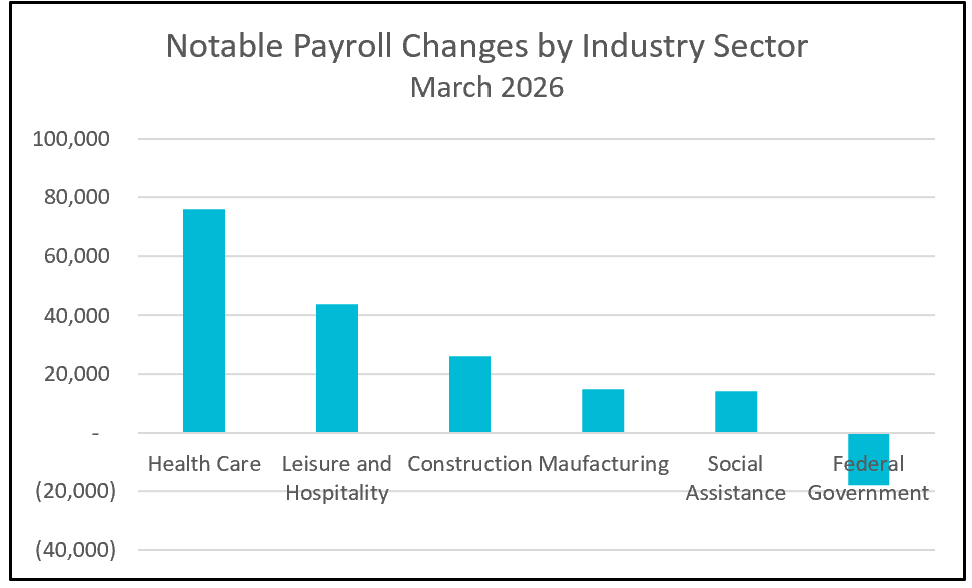

Once again, healthcare led the way with an increase of 76,000 jobs. Other sectors show less consistent strength: construction and manufacturing posted gains, but both have struggled in recent months, with manufacturing shedding jobs in most of the past year. Meanwhile, jobs declined in financial services and continued to contract in the federal government, where employment has fallen sharply since late 2024.

Sector-level trends further highlight this mixed outlook. While hiring gains were relatively broad-based in March, the labor market remains heavily dependent on healthcare and social assistance. Since 2025, these industries have driven most of the job growth. Payrolls have increased by 369,000 since the beginning of 2025. Jobs in health care and social assistance contributed 796,000 of those jobs, meaning that while more people were hired in health care, other sectors were reducing their payrolls.

Wage growth also reflects cooling momentum. Although hourly wages increased in March, the pace of growth was the slowest in nearly five years and barely kept up with inflation. (FRED) Average weekly earnings actually declined slightly due to a shorter workweek, adding pressure on household budgets—especially as higher gasoline prices erode purchasing power. These dynamics suggest that, despite stronger hiring, many workers are not experiencing meaningful real income gains.

Looking ahead, the report may overstate the economy’s strength because it does not fully capture the effects of the war in Iran, which began shortly before the survey period. Economists expect the conflict to weigh on labor demand through higher energy costs, disrupted supply chains, and increased business uncertainty, all of which could slow hiring in the months ahead. Softer consumer sentiment may further dampen demand for goods and services.

For policymakers, the report complicates the outlook. While the solid job gains reduce immediate concerns about an economic contraction, persistent inflationary pressures—particularly those stemming from rising energy prices—are likely to keep the Federal Reserve cautious. As a result, the Fed appears even less inclined to cut interest rates in the near term, prioritizing inflation control over economic stimulus.

The BLS will release March’s consumer price index on Friday. Higher Rock Education will post its analysis and summary shortly after the CPI is released.