I confess. I am an econ nerd. I see its relevancy everywhere. As a teacher, I am always trying to think of ways I can explain economic concepts using every day events not involving a business or money. Here are a few I have used in a classroom. I hope you find them helpful.

1. Supply and Demand

I am having a rough day. This morning I lost my glasses and searched an hour before I found them. On my way to work I realized that I had left my favorite pen at home. Not a big deal, I have several at the office.

I have one pair of glasses, and I cannot read without them. (In fact, I am not supposed to drive without them.) My demand for my glasses is very high. My supply is limited, so the price I am willing to pay for them – in terms of time I spent to search for them – is very high.

On the other hand, while I would have liked to use my favorite pen at work, I have several others. The supply was great, and my demand for my favorite pen was not sufficient for me to pay a high price i.e. return to the house to retrieve it.

Supply and demand is the most fundamental concept in economics. The price and quantity produced of a good or service is determined by the merging of the supply and demand. When supply is limited and the demand is high, the price is high. When the supply is great and the demand is low, the price is low. Visit any one of our eleven free

supply and demand lessons to learn more.

2. Competition or Monopoly

When I was a boy I loved to play soccer. I was not very good, so I tried to find a position where I could contribute. Goalie. No one wanted to play goalie. I had a monopoly on the position. I had very little competition, so I never worked very hard at improving. Unfortunately, that meant I did not improve much. In ninth grade I played on our junior high team. I was second string. I wanted to improve and practiced harder. I made it to first string. In high school I was demoted. My competition had worked very hard and attended several camps. He really was quite a bit better than I was I so I was relegated to the bench!

Competition makes us better. It also makes businesses better. Our economy is driven by competition. Businesses compete many ways: price, service, appearance, the accessories, cost, and more. Companies invest heavily to better their competition. Billions of dollars are spent annually to convince consumers that their good or service is better than the competition. Most companies invest large sums in technology to improve productivity and reduce their cost relative to their competition.

Sometimes companies do not have any competition. These are monopolies. The limited competition enables them to charge more for their good or service while investing less on improving. Learn more about the most fundamental economic assumptions at our free lesson:

Fundamental Economic Principles.

3. Ratchet Effect

Recently I finished reading the first novel by an author I have grown to like. I moved on to his second, and thoroughly enjoyed it. In fact, I would rank it among my favorites. The day after I finished his second novel I checked out his third from the library. Boy was I disappointed. It did not meet my expectations. It was good, probably comparable to the first book I read, but it sure did not reach my expectations after reading his second book. My expectations had be "ratcheted" higher. A ratchet is a tool such as a car jack or winch that prevents the item from slipping back. My expectations were ratcheted higher and I did not expect any slippage back to the level of satisfaction I received from reading the first book. Instead I expected the same higher level of satisfaction in the future.

Economists refer to the

ratchet effect when discussing price changes. When the economy is booming, manufacturers are quick to raise their prices. Workers are in a better position to demand higher wages. However, most companies do not reduce their prices as quickly as they raised them when the economy slows. These companies prefer cutting back on production rather than lowering their price. They also tend to lay off employees rather than reduce their wages. Prices and wages ratchet upward and are slower to drop.

To learn more about inflation and use an inflation calculator to compare prices visit our free lesson

Inflation.

4. Production Possibilities Frontier (PPF)

Rarely do I complete my "to do" list in a day. I am bad about thinking I can accomplish a chore in less time than it actually takes. Most frequently, if I devote all day to completing one task, I do not have enough time left to complete a second task. Other times, I may be productive only to be distracted and taken off task. In the first case, I am trying to reach beyond my capacity and accomplish the impossible – given my limited time. In the second case, I am achieving less than my potential and wasting time.

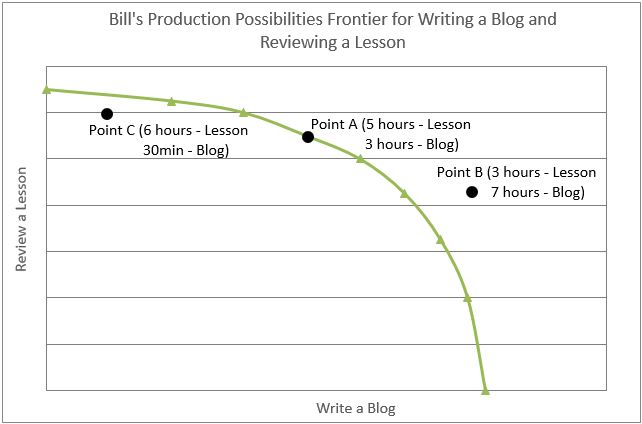

Today I have two goals: review a lesson, which I think will take five hours, and finish writing this blog which should take three hours. Unfortunately, the lesson has already taken six hours, so the blog will have to be finished tomorrow.

Economists use the production possibilities frontier to illustrate. On the X-axis I have placed writing a blog. Review the lesson is on the Y-axis. Point A is where I think I should be: five hours for the lesson and three hours for the blog. Notice that if I choose to spend more time on a lesson I must spend less time on the blog. Point B (three hours preparing the lesson and seven hours writing the blog) is outside of my possibilities. It is impossible for me to achieve my unrealistic objectives in an eight-hour day.

To make matters worse, a friend calls me up after I have just started the blog and suggests we go play nine holes of golf. I haven't seen my friend and it's awfully nice outside, so I choose to play golf. I am now operating inside my production possibilities frontier at point C where I have worked six hours on the lesson and 30 minutes on the blog.

The

production possibilities frontier provides a picture. Any point on the frontier is attainable, and our resources are being used efficiently. Outside the frontier is impossible to attain, given our limited resources. Inside the frontier represents a production level where the resources are not used efficiently. Watch our

video for the PPF where two members of a golf team debate how to allocate their time between studying and practicing and read our free lesson,

Production Possibilities Frontier, to learn more about relating the PPF to opportunity costs and a country's comparative advantage.

5. Comparative Advantage

Last night my wife and I decided to cook dinner together. We had steak, mashed potatoes, salad, and garlic bread. My wife is a much better cook than I am, plus she is very efficient. I can cook, but I am very deliberate. If I stayed inside and cut up the salad and mashed the potatoes it would take much longer to prepare our meal – plus I would probably get in her way. My wife is better at cooking steak. She knows the best seasoning. However, we determined that it would be most efficient if I cooked the steak. (That would also get me out of her way!) Cooking the steak was easy. All I needed to do was fire up the grill and throw on the meat. I also helped by setting the table.

Economists use

comparative advantage to describe how jobs should be divided. A team or country is the most efficient when each member or company operates where they have a comparative advantage. One person can have an

absolute advantage in each chore, as my wife did in cooking our meal last night. However, I had the comparative advantage in cooking the steak and setting the table because I could complete the task in about the same amount of time as my wife could.

Another example of comparative advantage is in defining roles in a band. Watch our

video to see what happens when our church band chooses to switch instruments.

You can also access our free lesson

Comparative Advantage and Specialization to learn more about how comparative advantage influences company mergers and international trade.

Please forward this blog to economics students and teachers you know. We plan to write Part II before the end of February. Please share any ideas of how everyday events are good examples of economic concepts that teachers can share with their students.